By Marcel Kasumovich, Deputy CIO of Coinbase Asset Administration

Crypto sparked a renaissance in real-time funds. Sleepy you say? Time for a wake-up name – cost options are on the chopping fringe of crypto’s integration into the mainstream, and it has loads of competitors.

“You’re in all probability used to crypto transactions, anticipating me to carry out one other visitor for an eight-minute commentary whereas we watch for affirmation. However that’s previous crypto. Are you prepared for the brand new crypto world? Watch very carefully…don’t blink…and that’s it,” John Collison exclaimed whereas illustrating a transaction on crypto rails with Stripe, a number one cost community that he co-founded. It was a seamless consumer expertise, in contrast to the corporate’s preliminary foray into bitcoin in 2014.

Each PayPal and Stripe at the moment are harnessing the ability of stablecoins into their acquainted consumer interfaces. This strategic transfer effortlessly brings customers onto the blockchain – level, click on, and it’s finished. It’s the brand new development, too. Conventional corporations are bringing customers onchain. There’s the crypto we see in noisy headlines and people working quietly to monetize the expertise, like PayPal and Stripe. They usually mix for a staggering 62% share of on-line cost software program processing.

Digital funds could not appear to be the thrilling promise of the longer term. But, they’re on the leading edge. Digital funds are taking a rising share of a quickly rising market because the world strikes away from money. International funds are measured within the hundreds of trillions, and the digital cost market has risen from a modest $10 billion in 2017 to a projected $200 billion in 2030. All of us dwell it, and the majority of the transactions are small worth, a espresso right here, a donut there.

The method is so seamless that we seldom pause to contemplate the way it really works. Poorly, because it occurs. Customers count on to have the ability to pay every time it’s handy. Settling your restaurant invoice, you don’t care that it’s exterior of banking hours. You simply desire a easy type of cost – and that’s not money. In the course of the time between you tapping your card and accounts being settled, a intermediary offers credit score to ensure all of it clears. And it’s costly at 2.3% of transaction worth.

One man’s revenue margin is one other’s invitation to disrupt. The standard narrative of disruption entails a wildly profitable firm dropping its innovation edge, and lacking market inflection factors. Polaroid made the primary instantaneous digicam in 1948 and dominated markets from floppy disks to movie. Income peaked in 1991 and the corporate was unable to pivot to the brand new digital period, declaring chapter ten years later. Studying from such histories, corporations at the moment are extra adaptive.

We see this clearly in funds. Effectivity is exactly what introduced PayPal and Stripe again to crypto. Transaction speeds have improved exponentially, now clocking at milliseconds, and prices have plunged to fractions of a cent. It helps that crypto tech fails quick – revealing resilience and weak point shortly. As an illustration, the resilience of USDC is now supporting its entry into the mainstream whereas Bored Apes Yacht Membership weak point persists, down 90% off earlier cycle highs.

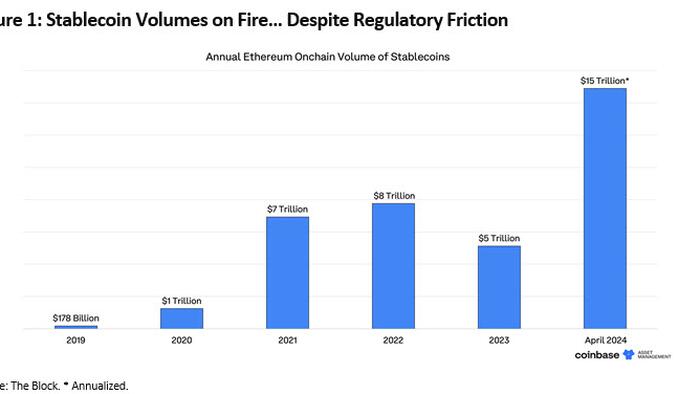

Why now? Why not! Stablecoins are demonstrating their prowess as cost instruments. Transaction volumes are monitoring new highs this month, operating at ~$15 trillion annualized on Ethereum alone (Determine 1). The effectivity acquire is obvious – instantaneous and last settlements imply that your late-night espresso and donut purchases bypass the necessity for credit score intermediaries. The intermediary is useless, though residing vibrantly via instruments like Stripe that ship customers a well-recognized expertise.

Customers don’t care that it’s crypto. They need an amazing expertise. Companies don’t care, both. They’re optimizing working effectivity for revenue. As crypto matures, so too does its worth proposition. Crypto is the protagonist of actual time funds and like several nice innovation, it fosters competitors. What’s distinctive with funds is that the competitors comes from each personal and authorities organizations, with regulatory stagnation working in favor of each.

Look past areas historically seen as leaders in innovation. The US stays a beacon of artistic expertise behind innovation. However customers are transferring slowly, lagging in fintech adoption. In spite of everything, US customers are accustomed to charges, don’t thoughts the service, and paying for factors on costly intermediation is a pastime. Actual-time settlement techniques adopted, like FedNow, are for enterprise functions, not for shoppers. It’s new gamers like India on the leading edge.

The Unified Cost Interface (UPI), India’s real-time cost answer, was developed by the central financial institution in 2016. It integrates peer-to-peer real-time funds, straight competing with crypto applied sciences. Final 12 months, UPI integrated 522 industrial banks overlaying 300 million lively customers and 117 billion transactions. Totally different from developed areas, intermediaries weren’t disrupted as these are largely new customers. Money was disrupted on the expense of the central financial institution.

Funds stand on the chopping fringe of crypto’s future. Consumer expertise is paramount. Integrating into the regulatory mainstream will speed up customers onchain, simply as service suppliers did for the web. Crypto unlocked the real-time settlement innovation, however will face competitors. It’s a world that argues for being chain-agnostic. The information between Ethereum, Bitcoin and UPI will combine to the very best of requirements and safety. That’s the street to creating onchain the brand new on-line.

Loading…

{kind=link}