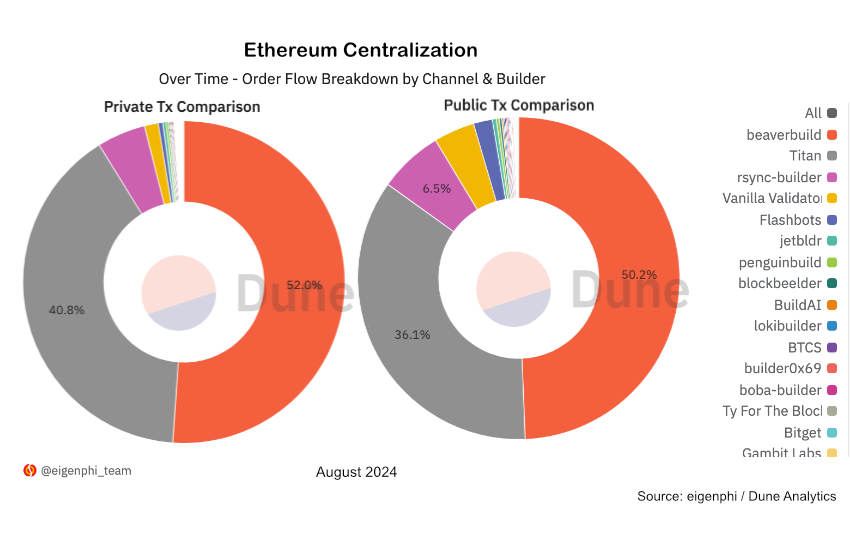

One of the numerous objectives of the 2022 Ethereum Merge was to make Ethereum extra decentralized. From a validator perspective, it’s not doing badly. Statistics present Coinbase is the biggest, controlling virtually 12% of staked ETH (though some declare it’s nearer to 30%). Nonetheless, validators don’t create the content material of the blocks. Block builders are those who embrace transactions, resolve on their order after which bid within the public sale to get their block included. This month a single block builder, Beaverbuild, has constructed more than half of Ethereum’s blocks.

Over 85% of blocks have been constructed by the highest two builders, and greater than 90% by the highest three.

This drive in direction of centralization is pushed by maximal extractable worth (MEV) the place the block builder reorders transactions to achieve a bonus. This normally includes a mixture of entrance working pending transactions and arbitrage.

Previously all pending Ethereum transactions have been publicly seen and block builders would choose transactions and construct blocks. Nonetheless, in a need to keep away from others seeing transactions, excessive frequency merchants (and different bot operators) have direct relationships with block builders, sending their transactions to them privately. These transactions are solely non-public within the pending state.

Current research from blocknative discovered that greater than half of Ethereum gasoline charges at the moment are paid by these non-public blocks, and these blocks account for 30% of all blocks.

This centralization of the block constructing operate was predicted early final 12 months in a paper printed by the Particular Mechanism Group (now half of Consensys). The group has proposed one of the potential options to deal with the problem.

Excessive frequency merchants drive centralization

They predicted that top frequency merchants (HFTs) would need to use non-public transactions and the potential income imply the related block builder can outbid different builders. Particularly, HFTs are likely to arbitrage between costs on centralized exchanges (CEXs) comparable to Binance and decentralized exchanges (DEXs) comparable to Uniswap. HFTs need to guarantee their transactions come on the high of the block, for which they’re keen to pay handsomely.

Beaverbuild was recognized as one of the HFTs, and EigenPhi claims that Symbolic Capital Companions is the HFT related to Beaverbuild.

Some other participant who desires to make sure their transactions are within the successful block is more likely to go on to Beaverbuild. In any case, they account for greater than half of successful blocks. Failing that, they’d go to the quantity two, Titan. Given the proposed solutions are nonetheless on the analysis stage, the actual query is what could be executed quickly?

{kind=link}