Sun International Restricted (JSE:SUI) will improve its dividend on the 14th of April to ZAR2.37, which is 17% increased than final 12 months’s fee from the identical interval of ZAR2.03. This takes the annual fee to eight.8% of the present inventory worth, which is about common for the trade.

Check out our latest analysis for Sun International

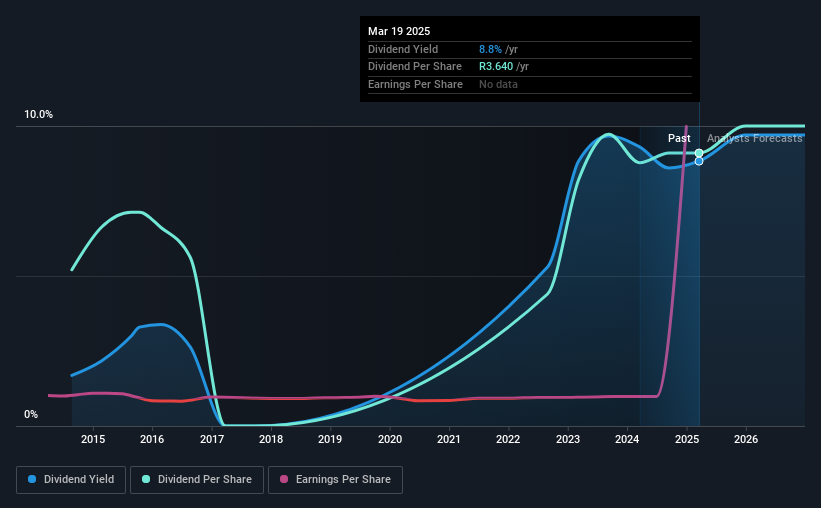

Sun International’s Future Dividend Projections Seem Nicely Lined By Earnings

We wish to see a wholesome dividend yield, however that’s solely useful to us if the fee can proceed. Earlier than this announcement, Sun International was paying out 88% of earnings, however a relatively small 43% of free money flows. This leaves loads of money for reinvestment into the enterprise.

Wanting ahead, earnings per share may rise by 9.1% over the following 12 months if the development from the previous couple of years continues. Assuming the dividend continues alongside the course it has been charting just lately, our estimates present the payout ratio being 74% which brings it into fairly a snug vary.

Dividend Volatility

Though the corporate has an extended dividend historical past, it has been lower at the very least as soon as within the final 10 years. The annual fee over the past 10 years was ZAR2.08 in 2015, and the latest fiscal 12 months fee was ZAR3.64. This suggests that the corporate grew its distributions at a yearly price of about 5.7% over that period. It’s good to see the dividend rising at an honest price, however the dividend has been lower at the very least as soon as prior to now. Sun International might need put its home so as since then, however we stay cautious.

The Dividend Has Progress Potential

On condition that the dividend has been lower prior to now, we have to examine if earnings are rising and if which may result in stronger dividends sooner or later. Sun International has seen EPS rising for the final 5 years, at 9.1% every year. Not too long ago, the corporate has been capable of develop earnings at an honest price, however with the payout ratio on the upper finish we do not suppose the dividend has many prospects for development.

In Abstract

In abstract, whereas it is all the time good to see the dividend being raised, we do not suppose Sun International’s funds are rock strong. The corporate is producing loads of money, which may preserve the dividend for some time, however the observe file hasn’t been nice. We do not suppose Sun International is a good inventory so as to add to your portfolio if earnings is your focus.

It’s necessary to notice that firms having a constant dividend coverage will generate higher investor confidence than these having an erratic one. Nonetheless, traders want to contemplate a bunch of different elements, aside from dividend funds, when analysing an organization. As an illustration, we have picked out 2 warning signs for Sun International that traders ought to think about. Is Sun International not fairly the chance you have been in search of? Why not take a look at our selection of top dividend stocks.

When you’re trying to commerce Sun International, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With purchasers in over 200 international locations and territories, and entry to 160 markets, IBKR allows you to commerce shares, choices, futures, foreign exchange, bonds and funds from a single built-in account.

Take pleasure in no hidden charges, no account minimums, and FX conversion charges as little as 0.03%, much better than what most brokers provide.

Sponsored Content material

New: Handle All Your Inventory Portfolios in One Place

We have created the final portfolio companion for inventory traders, and it is free.

• Join an infinite variety of Portfolios and see your whole in a single foreign money

• Be alerted to new Warning Indicators or Dangers through e-mail or cellular

• Observe the Honest Worth of your shares

Have suggestions on this text? Involved concerning the content material? Get in touch with us instantly. Alternatively, e-mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary primarily based on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles aren’t supposed to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary scenario. We purpose to deliver you long-term centered evaluation pushed by elementary information. Notice that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

{kind=link}