As the Trump administration fast-tracks stablecoin regulation, analysts are starting to foretell surging demand for U.S. Treasurys.

This story was featured in Difficulty 17 of Forbes Australia. Tap here to safe your copy.

Brian Moynihan, the chief govt officer of $2.6 trillion (property) Financial institution of America, doesn’t normally make headlines for his crypto opinions. However in February, he did simply that: “In the event that they make that authorized, we’ll go into that enterprise.” He was speaking about stablecoins—blockchain-based tokens usually pegged to the U.S. greenback and, more and more, the plumbing of world funds. “They” are Congress, which is now racing to put down the guidelines of the highway for these crypto creations.

The STABLE Act in the Home and the GENIUS Act in the Senate are dueling payments with a standard objective: to deliver stablecoin issuers into the regulatory fold, spelling out precisely how a lot capital, liquidity and danger administration is sufficient. In addition they intention to make clear which federal or state businesses get to play referee. However there’s one other, much less flashy subplot: how will widespread acceptance of stablecoins amongst conventional establishments globally have an effect on the $28 trillion United States Treasury market?

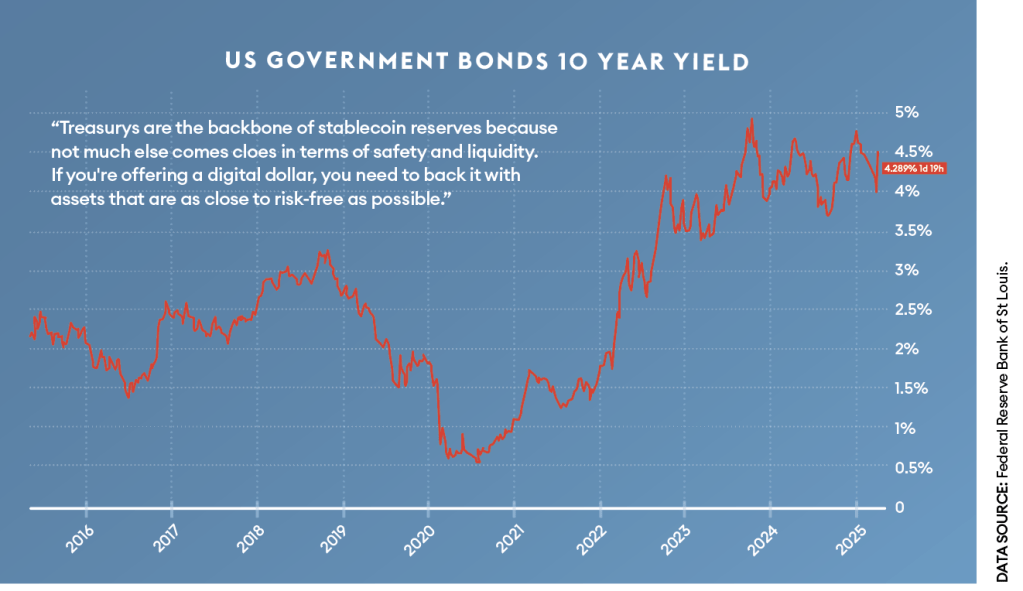

Right here’s the factor: Treasurys are the spine of stablecoin reserves as a result of not a lot else comes shut when it comes to security and liquidity. Should you’re providing a digital greenback, you should again it with property that are as near risk-free as doable. This sounds rather a lot like tons of of cash market mutual funds, which are issued by giants like BlackRock, Constancy and Vanguard and maintain over $6 trillion in property, largely in U.S. Treasury payments. The large distinction is that not like a cash market fund, say, from Constancy, which could pay you an annual yield of 4%, most stablecoin issuers have to this point resisted providing any sort of yield or earnings to their holders. That’s one purpose why Tether, the largest of them, has extraordinarily excessive margins and reported over $1 billion in working revenue in the first quarter of 2025.

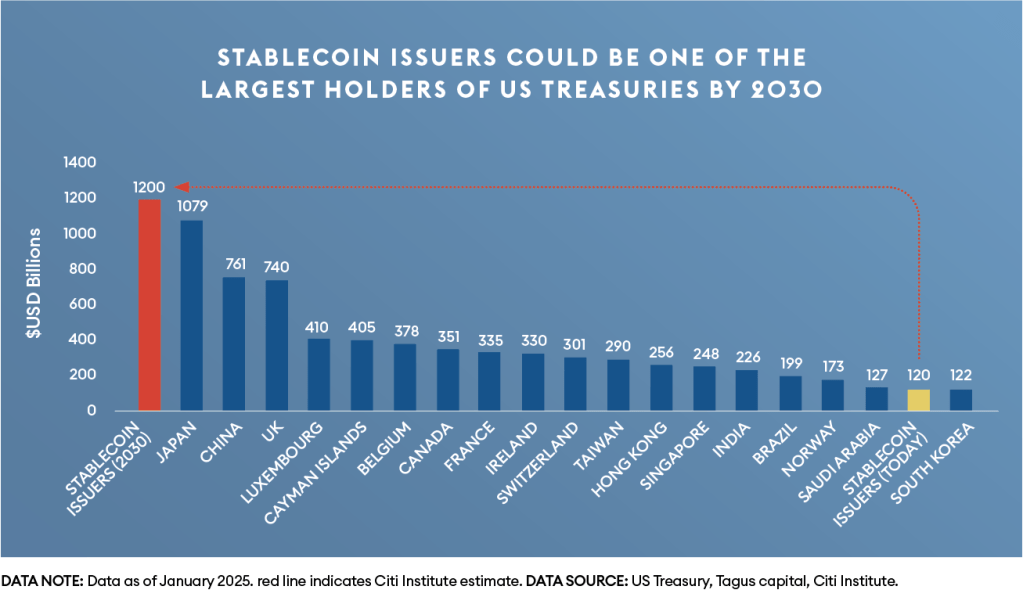

Proper now, the dozens of stablecoin issuers that exist—although largely Tether, primarily based in El Salvador, and Circle, headquartered in New York—maintain an estimated $150 billion in U.S. authorities debt, primarily short-term T-bills. That’s a rounding error in the $28 trillion Treasury securities market and a reasonably insignificant portion of the $6 trillion in Treasury payments excellent. Most Treasurys are nonetheless held by the U.S. authorities itself, assume Social Safety and federal pension funds. U.S. mutual funds, banks and insurance coverage corporations are the subsequent greatest holders, with international buyers accounting for about 30% (roughly $8.8 trillion), led by Japan and China.

However Britain’s Customary Chartered Financial institution, an $874 billion (property) establishment that provides custody for cryptocurrencies, tasks that the international stablecoin market may bounce from $240 billion to $2 trillion in simply three years. Each present drafts of the stablecoin payments explicitly establish Treasury securities with maturities of 93 days or much less as one in every of the few acceptable reserves. That might imply an additional $1 trillion in demand for T-bills in the close to time period, in keeping with an April 30 presentation by the Treasury Borrowing Advisory Committee (TBAC), a gaggle of senior bankers, asset managers and hedge fund representatives that advises Treasury officers every quarter. Citi’s analysis crew goes additional, suggesting that by 2030 stablecoin issuers may surpass any single international nation as holders of U.S. authorities debt. Regardless of its controversial historical past, Tether, with $120 billion invested in U.S. Treasurys already, may turn out to be the largest holder if it falls into compliance with new rules.

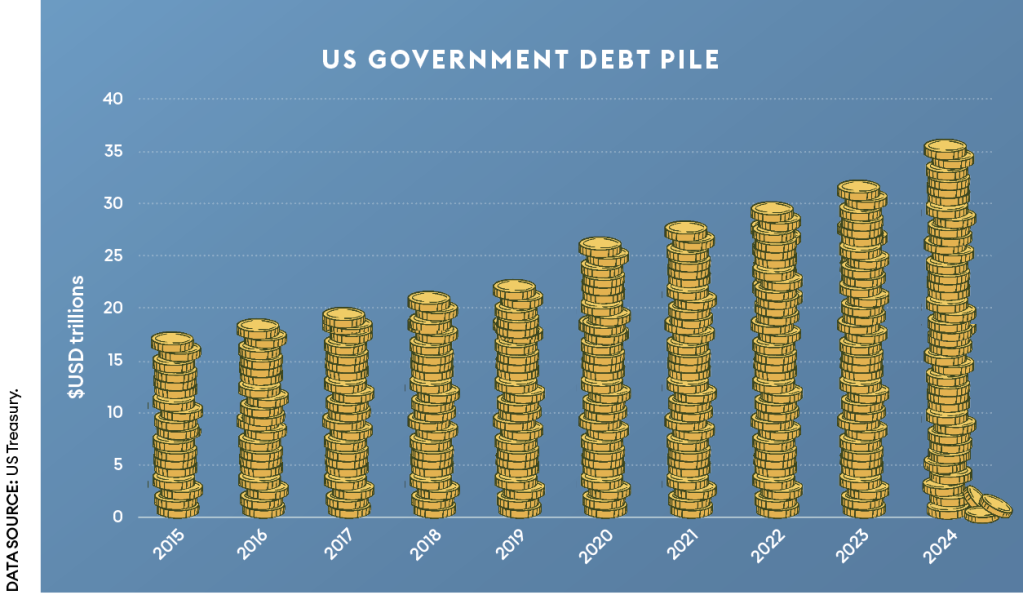

This market upheaval may unfold as the U.S. nationwide debt climbs previous $36 trillion, swelling by one other trillion roughly every 176 days. In the meantime, collectors like China and Saudi Arabia are quietly trimming their Treasury holdings. China’s dropped to $761 billion earlier this 12 months, its lowest since 2009, whereas Saudi Arabia’s have fallen to a year-and-a-half low of $126 billion, reflecting a worldwide rebalancing of reserves and rising skepticism about U.S. sovereign debt. Enter crypto customers round the world, in locations like Buenos Aires and Nairobi, utilizing stablecoins for every little thing from paying their hire to hedging in opposition to native foreign money volatility and concurrently stepping up as a brand new, keen class of lenders to Uncle Sam.

The Trump administration has already made its stance on stablecoins clear. Crypto and AI Czar David Sacks has argued that they may assist safe the greenback’s international dominance, and President Trump has pressed Congress to get a invoice to his desk earlier than the August recess.

“Stablecoins have the potential to make sure American greenback dominance internationally to extend the utilization of the U.S. greenback digitally as the world’s reserve foreign money, and in the course of create doubtlessly trillions of {dollars} of demand for U.S. Treasuries, which may decrease long-term rates of interest,” stated Sacks throughout his first press convention in February.

Moreover, the Trump household’s crypto enterprise, World Liberty Monetary, introduced plans for its personal stablecoin, which is now apparently complicating the destiny of pending regulation. On Could 1, World Liberty introduced that the token can be utilized by MGX, an Abu Dhabi government-backed agency, to take a position $2 billion into Binance, the crypto trade whose founder is reportedly in search of a presidential pardon. A few days later, 9 Senate Democrats, together with 4 who beforehand backed the stablecoin “GENIUS” invoice, issued a press release saying they might oppose the laws in its present kind, Politico reported.

However lawmakers had been selling the concept of stablecoin issuers as final Treasurys consumers even earlier than Trump took workplace. Congressman Ritchie Torres of New York wrote final fall that extra stablecoin adoption means greater demand for Treasurys and, in flip, decrease U.S. borrowing prices. Earlier, former Home Speaker Paul Ryan floated stablecoins as a buffer in opposition to a future wave of international promoting: if conventional consumers retreat, dollar-backed token issuers may fill the hole.

Christopher Perkins, president of crypto-focused funding agency CoinFund, places it bluntly: “You couldn’t invent a greater innovation for the U.S. greenback than a stablecoin. It makes the greenback extra accessible globally. It reinforces it as the international reserve foreign money. If it will get into the mistaken arms, there’s due course of by which the authorities can freeze and seize property. It checks so many bins: creates consumers for your debt, brings your rates of interest decrease.”

Yesha Yadav, a professor at Vanderbilt College whose analysis focuses on the Treasury market, is decidedly much less enthusiastic a few crypto takeover of the authorities securities market. She believes that embedding stablecoins into it creates new vulnerabilities. “If the U.S. Treasury market turns into, for no matter purpose, pressured, if there are doubts about the U.S.’s means to make good on its funds, then for stablecoin issuers, it’s now not a secure asset that may substitute as a cash declare,” she explains.

And if a significant stablecoin issuer collapses, it may very well be compelled to dump Treasurys en masse, destabilizing the market. Not like international central banks, stablecoin issuers face real run danger: panicked clients can pull funds immediately, triggering rapid promoting strain. In fact, this danger applies to cash market funds as properly. In 2008, after Lehman Brothers collapsed, the $65 billion Reserve Main Fund, which held lower than 2% of Lehman’s business paper, skilled a run and “broke the buck”, forcing it to liquidate its property.

“For the first time, the Treasury market is supporting the moneyness of a fee system by changing into a backstop of a completely new financial declare,” Yadav notes. If a disaster hits, will the authorities must bail out stablecoin issuers to honor the greenback claims they’ve issued? Policymakers haven’t absolutely grappled with these questions, and they need to, she says.

Arthur Wilmarth, a legislation professor at the George Washington College, raises one other concern: “The creation of main new calls for for Treasury payments and Treasury-backed repos and reverse repos by stablecoin issuers may trigger harmful shortages of obtainable Treasury payments, notably during times of monetary stress.” He factors to previous disruptions like the repo market disaster of September 2019 and the “sprint for money” in March 2020 as cautionary tales.

For now, one other trillion {dollars} in Treasury demand from stablecoin issuers may appear manageable. However the panorama is shifting quick. Main monetary establishments like Financial institution of America and Constancy, which handle trillions in property, are eyeing stablecoin launches. Visa and Stripe-acquired Bridge simply rolled out stablecoin-linked playing cards throughout Latin America, and Mastercard unveiled a brand new platform by which customers will have the ability to pay for purchases with stablecoins and withdraw them straight into their financial institution accounts.

Nonetheless, Yadav cautions anybody pondering that stablecoins will turn out to be a dependable backstop for the U.S. greenback or the Treasury market: “The presumption that stablecoin issuers will merely fill the hole, shouldn’t be one thing that policymakers ought to be relying on,” she warns.

And there’s one other potential danger: will banks and different stablecoin issuers restrict their reserves to Treasurys? Kevin Lehtiniitty, CEO of Borderless.xyz, believes bank-issued stablecoins may turn out to be topic to the fractional reserve guidelines that banks have lengthy used to show their FDIC-insured deposits into extra profitable development areas. Maybe, business actual property, subprime mortgages, DeFi? Keep tuned.

‘Fast Takes’ featured in Difficulty 17 of Forbes Australia. Tap here to safe your copy.

Look again on the week that was with hand-picked articles from Australia and round the world. Sign up to the Forbes Australia newsletter here or become a member here.

{kind=link}