Introduction

Base, created by crypto alternate Coinbase, is the highest revenue-generating Ethereum layer-2 (L2), typically outearning all different high rollups mixed each day. During the last 180 days, Base has earned a median of $185,291 in each day income, dwarfing Arbitrum’s (the No. 2 revenue-generating L2) $55,025 each day common income, and the mixed each day common income of $46,742 of the subsequent 14 high rollups by total value secured.

It’s clear Base has emerged as a persistently excessive revenue-generator, however what’s driving the financial exercise? And what does Base have that different main L2s shouldn’t have that allows such worth era?

This report explores Base’s payment panorama and highlights the exercise driving its income. We discover that Base’s sequencing mannequin and decentralized alternate (DEX) exercise are the important thing drivers.

Base’s Sequencing Mannequin

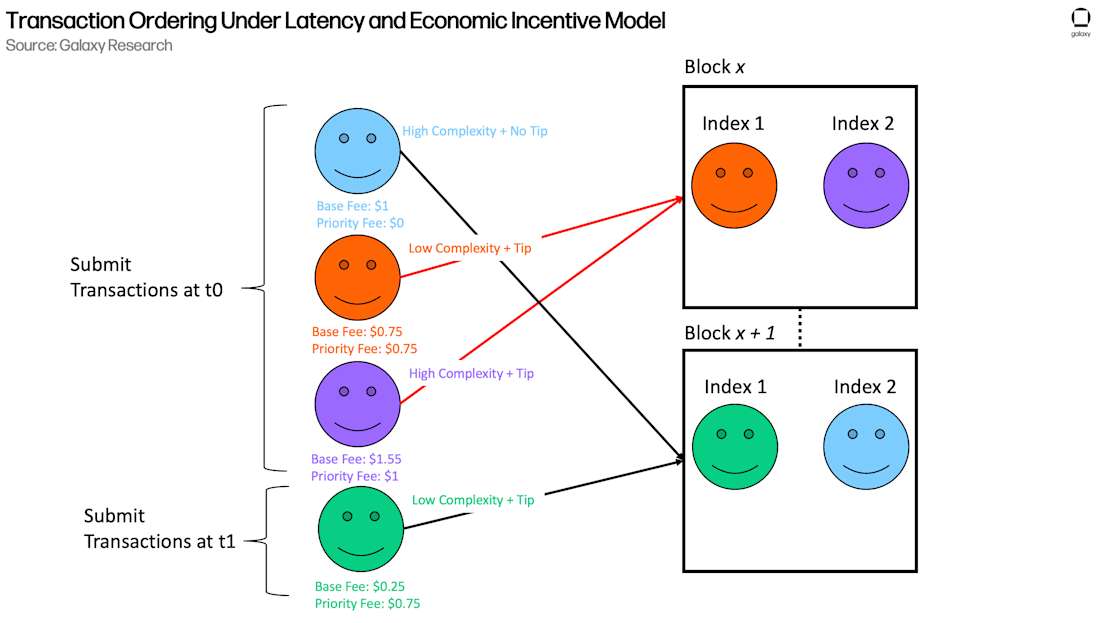

Transaction ordering on Base is set by two variables:

-

when transactions are submitted (latency); and

-

how a lot the sender pays in charges relative to the complexity of the transaction (financial incentive)

This setup is just like how transport companies like UPS function: they ship packages as people drop them off and give senders the choice to pay further for “categorical” transport that grants sooner supply. The precedence payment mechanism creates a dynamic public sale that mirrors the rules of Ethereum’s EIP-1559 payment mannequin, balancing arrival time with financial incentives.

To seize this, transactions on Base carry a “base” payment (small “b,” to not be conflated with the title of the chain) and a precedence payment; all customers pay the bottom payment to ship transactions whereas the precedence payment is elective and required just for expedited execution.

However how does the sequencer determine which “categorical” bundle to prioritize? It does not think about the whole payment outright; it appears to be like on the payment supplied per unit of gasoline (computation required), or how worthwhile a transaction is for the quantity of sources it requires to execute.

Let’s revisit the transport firm analogy. Think about the supply truck has a restricted quantity of house (the block’s gasoline restrict). The driving force (the sequencer) needs to maximise her ideas for the house obtainable. She is introduced with two packages:

-

A big bundle (a resource-intensive transaction) with a base transport payment of $50, however solely a $10 precedence tip. It takes up half the truck.

-

A small bundle (a easy transaction) with a base transport payment of solely $20, and a $10 precedence tip as properly. It takes up little house.

The driving force will all the time load the small bundle first regardless of the whole payment it pays being $30 lower than that of the massive bundle, as a result of it’s much more worthwhile for the house it occupies.

The sequencer on Base does the identical, prioritizing transactions that provide the best precedence payment per unit of gasoline consumed, thereby making certain probably the most computationally “costly” block can be probably the most worthwhile. Due to this fact, of two customers who submit transactions on the similar time, whoever pays the upper precedence payment per gasoline consumed is the one who’s most probably to get their transaction included first, whatever the transaction’s complexity or its complete payment paid.

The graphic beneath illustrates what this course of appears to be like like.

Why This Issues and How Base Differs from Competing Chains

Base’s EIP-1559-style payment mannequin creates a steady, open-market public sale for block house the place customers instantly bid for inclusion in line with their transaction’s urgency and/or profitability. Consequently, whereas there may be nonetheless a side of latency competitors, the financial leg permits income for the sequencer to scale instantly with the demand for block house and the profitability of transactions on the chain.

This differs from Arbitrum’s essential sequencing mechanism, for instance, which orders transactions strictly on a primary come, first serve (FCFS) foundation, and customers are primarily competing on latency as an alternative of financial price. On this mannequin, the first competitors isn’t over who pays extra, as a result of the payment per gasoline of all customers is similar and precedence charges will not be used, however who can get their transaction to the sequencer the quickest. This creates a “latency race,” the place subtle actors put money into low-latency infrastructure to make sure their transactions are processed first. On this setting, the one aggressive benefit is pace, as a result of there isn’t a mechanism to pay a premium for the next spot within the execution queue. This FCFS mannequin signifies that charges on Arbitrum scale with the magnitude of demand, however not as successfully with the profitability or urgency of any single transaction.

In April 2025, Arbitrum launched Timeboost to create a extra fluid FCFS-based system that enables the sequencer to seize priority-like income. Successfully, Timeboost added an execution categorical lane on Arbitrum that customers bid to entry for a restricted time. Customers with entry to the categorical lane get near-instant execution whereas everybody else continues to be ordered on a FCFS foundation with a slight (200 millisecond) delay to compensate for the categorical lane. Whereas Timeboost introduces a type of precedence bidding, its mechanism is extra predictive than reactive in comparison with Base’s precedence fee-based mannequin. Bidders should predict the whole potential revenue of a future time slot and bid primarily based on their estimates. This implies Arbitrum receives a hard and fast payment from the successful bidder, no matter how worthwhile that slot seems to be. This proactive, fixed-rate mannequin is much less efficient at capturing the worth of sudden, high-profit moments than a reactive system the place customers bid on every transaction individually.

How A lot Income Is Base Producing?

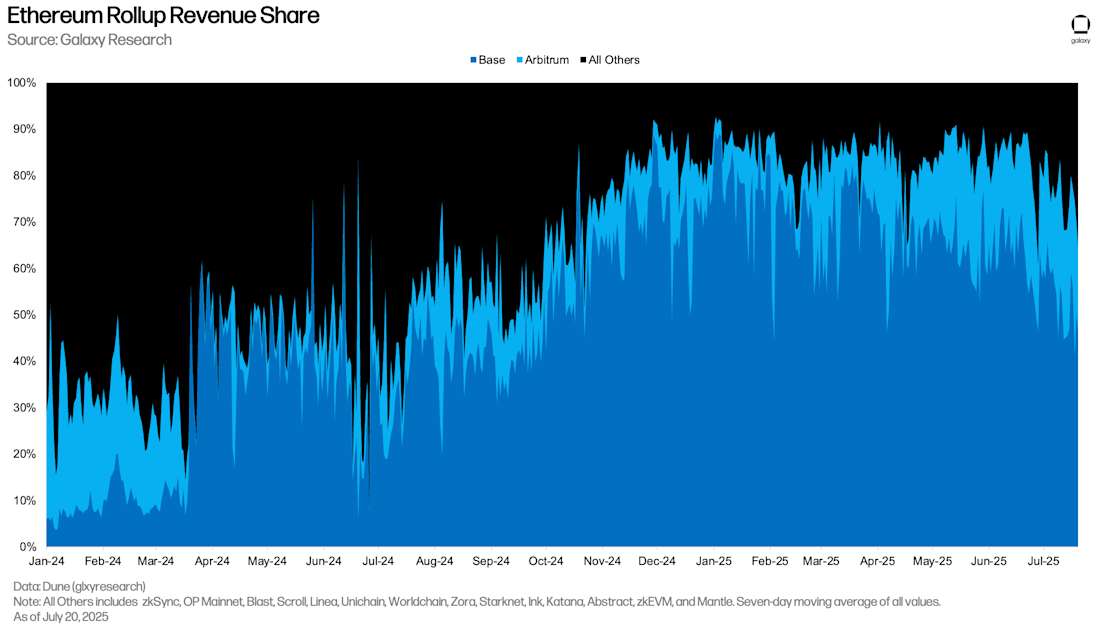

During the last 180 days, Base has generated a median of $185,291 in each day income. This compares to Arbitrum’s $55,025 and the summed each day common of 14 different Ethereum L2s’ $46,742 each day income.

12 months-to-date (YTD), Base has generated $33.4 million in income, Arbitrum has generated $9.9 million, and the 14 different L2s generated $8.4 million in income.

On a relative foundation, Base has captured 64% of the income generated by 15 of the highest Ethereum L2s by complete worth secured over the past 180 days. Its share has grown considerably over the past yr, increasing by as a lot as 48 share factors from its 37% each day common in July of 2024 utilizing the seven-day transferring common of each day income share. As of July 20, Base’s share of Ethereum rollup income has compressed to 49.7% as exercise has ramped up throughout different chains.

Priority Fees Play a Large Position

Transaction charges on Base have two main elements and an elective precedence payment:

-

Layer-1 (L1) payment: this covers the price of posting a batch of L2 transactions to the Ethereum mainnet. After Ethereum’s Pectra improve in March 2024, which enabled blobs through EIP-4844, the L1 payment element of Base (and L2 transactions usually) declined considerably. That is because of the larger financial effectivity of posting batch knowledge via blobs in comparison with posting them as name knowledge in L1 transactions.

-

Base payment: the obligatory, algorithmically decided payment for executing a transaction on Base. It’s set by the protocol and fluctuates relying on how full the final block was. When the community will get busier, the bottom payment will increase, and when it is much less busy, it decreases.

-

Priority payment: an elective payment, additionally known as a “tip,” that may be included to prioritize the execution of a transaction. Priority charges may help get transactions in greater positions in a block or be certain a transaction is included within the present block and not held up for the subsequent. There might be hundreds of transactions in a single block, that are executed in sequential order primarily based on their “slot” place. Sometimes, the highest slot of the block is probably the most worthwhile as a result of the transaction in that place is executed first and is undisturbed by any subsequent transactions.

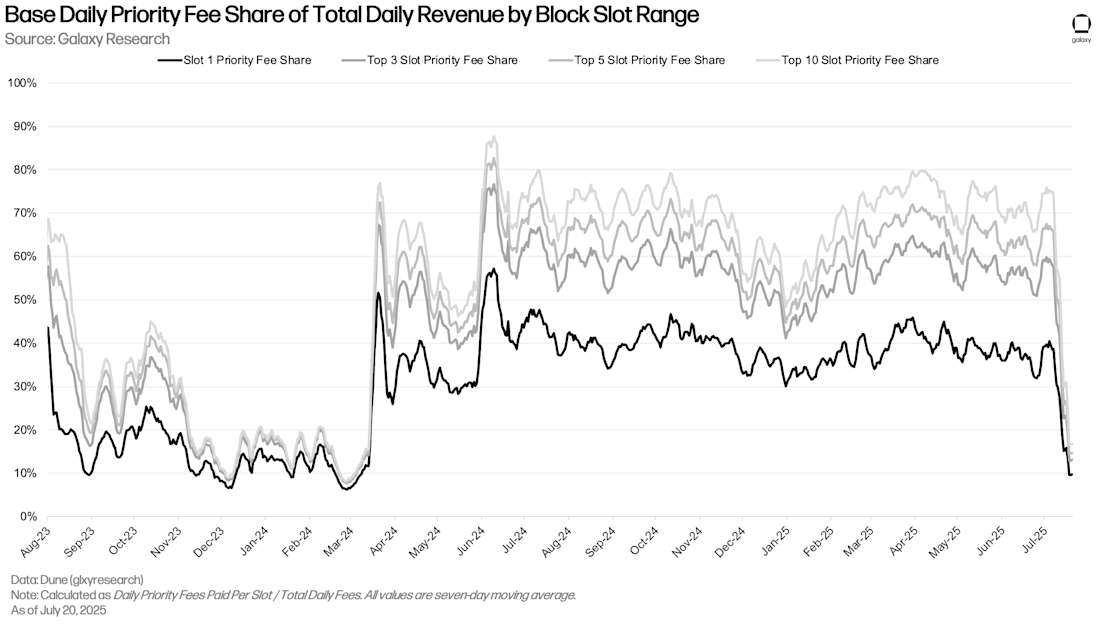

Priority charges are a serious contributor to the income generated by Base, with customers bidding for expedited execution. During the last 180 days, Base has earned a median of $156,138 in precedence charges each day, which comprised a median of 86.1% of its each day income.

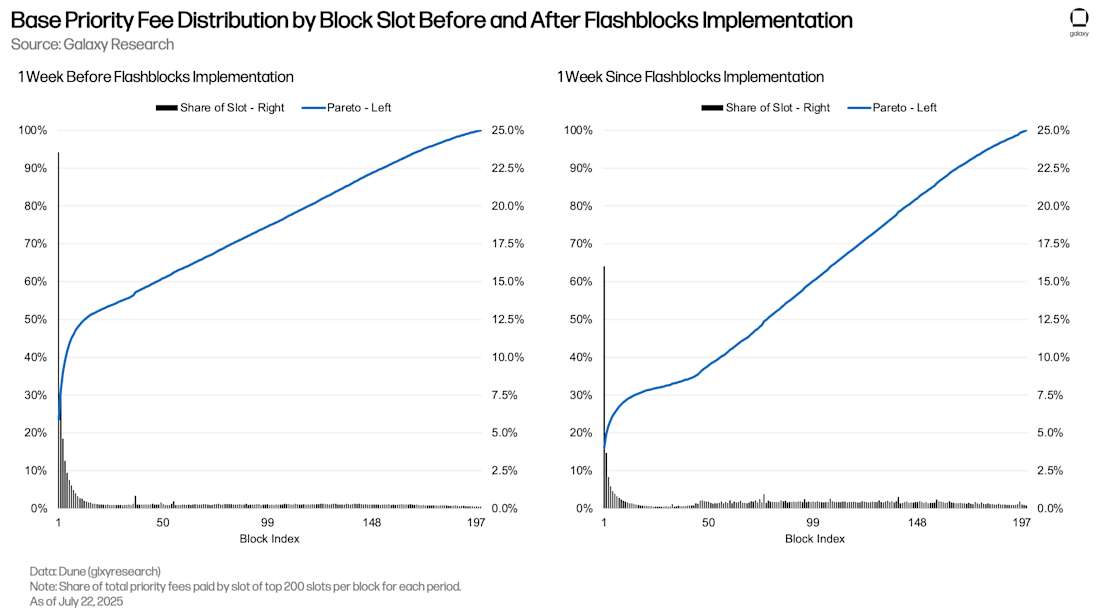

Particularly, precedence charges paid within the high slots of Base blocks have been large contributors to sequencer income from customers competing for inclusion close to the highest of the block. Priority charges paid by transactions within the high (first) slot of the block alone have contributed 30% to 45% of each day income in 2025 YTD. Furthermore, the precedence charges paid by transactions within the high 10 slots of every block contributed 50% to 80% of each day income over the identical interval. Nevertheless, top-slot precedence charges’ share of complete each day income has declined sharply within the weeks following July 5. This is because of two components: 1) elevated visitors driving base charges greater, in flip diluting the share of income stemming from precedence charges, and 2) the implementation of Flashblocks (described beneath) on July 16, which has resulted in high-priority transactions touchdown in decrease slots of blocks (which, as we’ll see, isn’t as disappointing because it sounds).

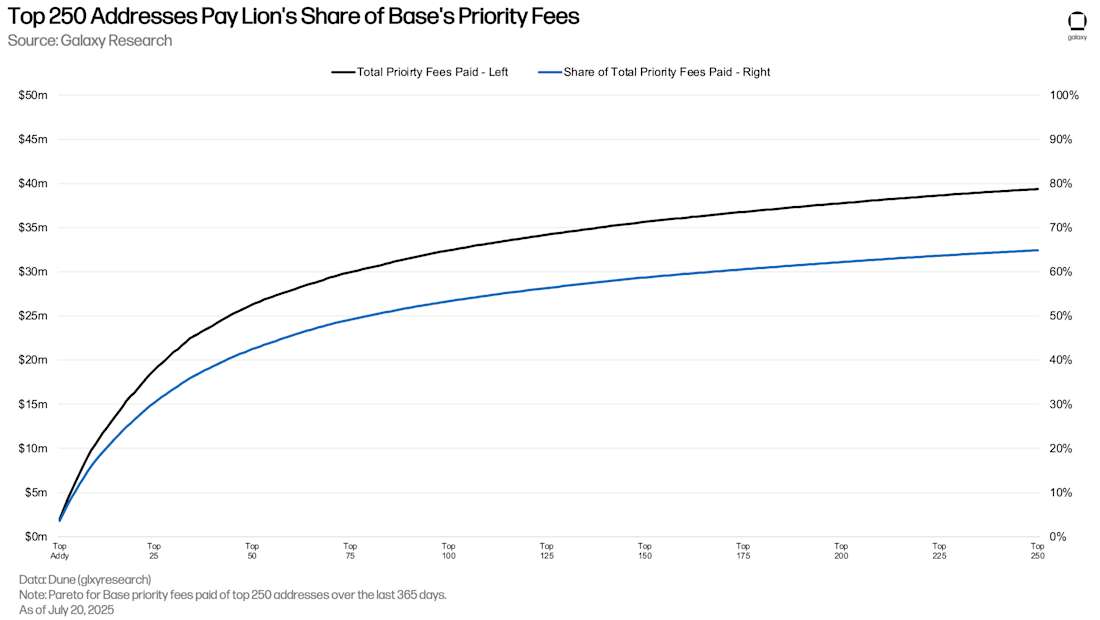

The precedence charges paid largely come from a small group of addresses, with 64.9% of all precedence charges paid over the past yr coming from simply 250 addresses. The highest handle alone paid 3.6% of all precedence charges over this time, which equated to $1.99 million primarily based on the value of ether on the time charges have been paid.

What’s Flashblocks?

Flashblocks, developed by Flashbots, goals to enhance the processing pace of transactions on Base. To realize this, it introduces “sub-blocks” that are high-confidence pre-confirmations of subsections of blocks which might be created each ~200 milliseconds. For instance, a single block can have three distinct subsections that customers get transaction pre-confirmations on earlier than the block is confirmed onchain at its set two-second interval. This makes transactions really feel nearly instantaneous to the end-user regardless of the Base block interval going unchanged, making a a lot smoother and extra responsive expertise.

Why is that this vital to the Base community payment evaluation by slot? As a result of every “sub-block” is successfully handled as a brand new block from the angle of transaction ordering. Consequently, excessive precedence payment transactions can fall to decrease slots of the general “confirmed block” however be on the high of the “pre-confirmed sub-block.”

This concept is visualized beneath within the divergence within the distribution of precedence charges paid for the primary 200 block slots earlier than and after Flashblocks’ implementation. The black bars characterize every particular person slot’s share of precedence charges; the blue traces characterize the cumulative share of all slots as much as that time (the Pareto distribution).

Within the week main into Flashblocks, the Pareto was steep via the primary ten slots, then grew extra linearly towards the two hundredth slot. In contrast, within the week following Flashblocks’ implementation, the Pareto is flatter on the lowest slots and steepens across the fiftieth slot of every block – that is the indication that prime precedence payment transactions are touchdown in later slots of the confirmed blocks.

Influence of Dex Swaps

Decentralized alternate (DEX) exercise is distinguished on Base. Of all of the Ethereum L2s, Base generates probably the most each day DEX quantity, occupying 50% to 65% of DEX quantity throughout L2s, and has the best DEX total value locked (TVL) of all of the L2s (excluding perpetual futures DEXes).

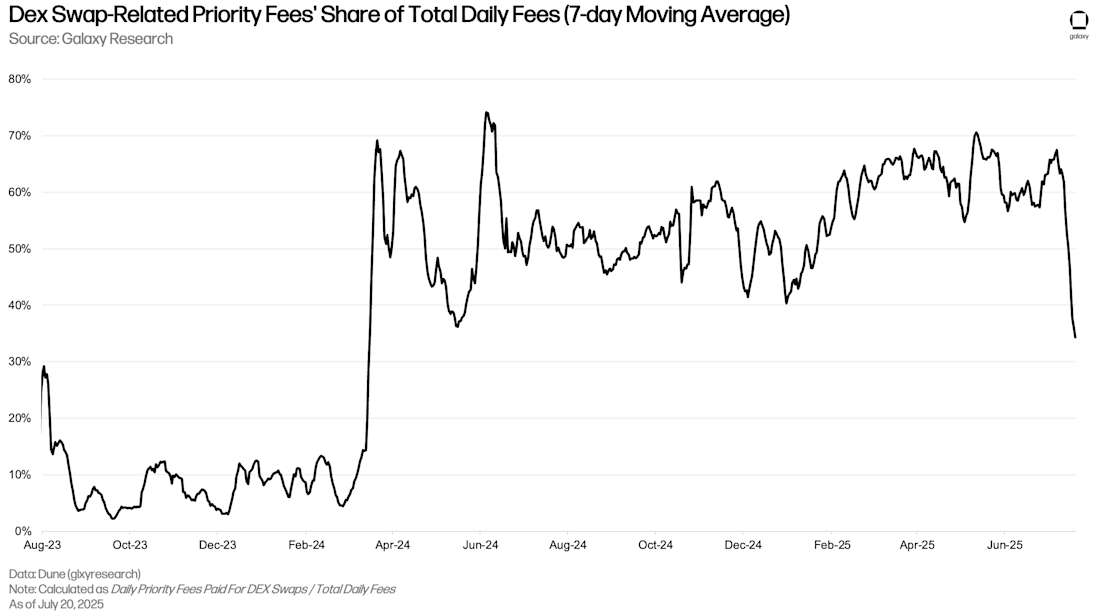

The prominence of DEX exercise is a driving issue for the elevated quantity of precedence charges paid on Base. Between 50% and 70% of the whole charges paid to the Base sequencer each day have stemmed from DEX swap precedence charges. Since July 7, nevertheless, DEX swap payment contribution to complete each day charges has fallen from 67% to only 34%. This may be attributed to a mix of precedence payment share dilution pushed by elevated base charges and a rise in competitors for block house throughout the chain, forcing customers so as to add precedence charges for non-DEX swap transactions.

The precedence charges paid by DEX swaps within the first slot alone have contributed 30% to 35% of complete precedence charges each day, and DEX swap precedence charges from the highest three slots contribute 50% to 62% of complete precedence charges each day to date in 2025. This reveals that high-urgency DEX swaps are a major contributor to Base income. The latest decline of DEX swap precedence charges from the highest slots of every block might be attributed to a mixture of larger rivalry throughout the chain forcing customers so as to add precedence charges for non-DEX swap transactions and Flashblocks, which may push high-priority DEX swaps into decrease slots within the block.

Conclusion

From surveying Base’s DeFi and income panorama, we see:

-

Priority charges making up the overwhelming majority of income

-

Greater than 60% of precedence charges paid over the past yr coming from simply 250 addresses

-

Excessive DEX volumes and TVL

-

Priority charges from DEX swaps contributing practically three quarters of all precedence charges paid

The end result of those factors means that most extractable worth (MEV) transactions, significantly aggressive actions like DEX arbitrage, are a major contributor to Base sequencer income. The sequencer’s EIP-1559 model payment mannequin is the direct mechanism for this; it transforms the competitors for block house from an inefficient, latency-based race into an environment friendly financial public sale.

By gathering precedence charges from customers prepared to pay for pressing inclusion, this mannequin permits the sequencer to instantly seize and monetize block house rivalry much more successfully than conventional “first come, first served” or purely latency-driven programs.

Authorized Disclosure:

This doc, and the knowledge contained herein, has been supplied to you by Galaxy Digital Inc. and its associates (“Galaxy Digital”) solely for informational functions. This doc might not be reproduced or redistributed in complete or partially, in any format, with out the categorical written approval of Galaxy Digital. Neither the knowledge, nor any opinion contained on this doc, constitutes a suggestion to purchase or promote, or a solicitation of a suggestion to purchase or promote, any advisory providers, securities, futures, choices or different monetary devices or to take part in any advisory providers or buying and selling technique. Nothing contained on this doc constitutes funding, authorized or tax recommendation or is an endorsement of any of the stablecoins talked about herein. It’s best to make your individual investigations and evaluations of the knowledge herein. Any choices primarily based on data contained on this doc are the only duty of the reader. Sure statements on this doc mirror Galaxy Digital’s views, estimates, opinions or predictions (which can be primarily based on proprietary fashions and assumptions, together with, particularly, Galaxy Digital’s views on the present and future marketplace for sure digital belongings), and there isn’t a assure that these views, estimates, opinions or predictions are presently correct or that they are going to be in the end realized. To the extent these assumptions or fashions will not be appropriate or circumstances change, the precise efficiency could fluctuate considerably from, and be lower than, the estimates included herein. None of Galaxy Digital nor any of its associates, shareholders, companions, members, administrators, officers, administration, workers or representatives makes any illustration or guarantee, categorical or implied, as to the accuracy or completeness of any of the knowledge or another data (whether or not communicated in written or oral kind) transmitted or made obtainable to you. Every of the aforementioned events expressly disclaims any and all legal responsibility referring to or ensuing from using this data. Sure data contained herein (together with monetary data) has been obtained from revealed and non-published sources. Such data has not been independently verified by Galaxy Digital and, Galaxy Digital, doesn’t assume duty for the accuracy of such data. Associates of Galaxy Digital could have owned, hedged and offered or could personal, hedge and promote investments in a few of the digital belongings, protocols, equities, or different monetary devices mentioned on this doc. Associates of Galaxy Digital can also lend to a few of the protocols mentioned on this doc, the underlying collateral of which might be the native token topic to liquidation within the occasion of a margin name or closeout. The financial results of closing out the protocol mortgage may instantly battle with different Galaxy associates that maintain investments in, and help, such token. Besides the place in any other case indicated, the knowledge on this doc is predicated on issues as they exist as of the date of preparation and not as of any future date, and won’t be up to date or in any other case revised to mirror data that subsequently turns into obtainable, or circumstances present or adjustments occurring after the date hereof. This doc offers hyperlinks to different Web sites that we expect may be of curiosity to you. Please be aware that once you click on on considered one of these hyperlinks, chances are you’ll be transferring to a supplier’s web site that isn’t related to Galaxy Digital. These linked websites and their suppliers will not be managed by us, and we aren’t liable for the contents or the right operation of any linked website. The inclusion of any hyperlink doesn’t suggest our endorsement or our adoption of the statements therein. We encourage you to learn the phrases of use and privateness statements of those linked websites as their insurance policies could differ from ours. The foregoing doesn’t represent a “analysis report” as outlined by FINRA Rule 2241 or a “debt analysis report” as outlined by FINRA Rule 2242 and was not ready by Galaxy Digital Companions LLC. Equally, the foregoing doesn’t represent a “analysis report” as outlined by CFTC Regulation 23.605(a)(9) and was not ready by Galaxy Derivatives LLC. For all inquiries, please e-mail [email protected]. ©Copyright Galaxy Digital Inc. 2025. All rights reserved.

{kind=link}