Written by: Liu Honglin

I do not know why, however these days, convention paperwork associated to the crypto {industry} appear to be launched on Fridays.

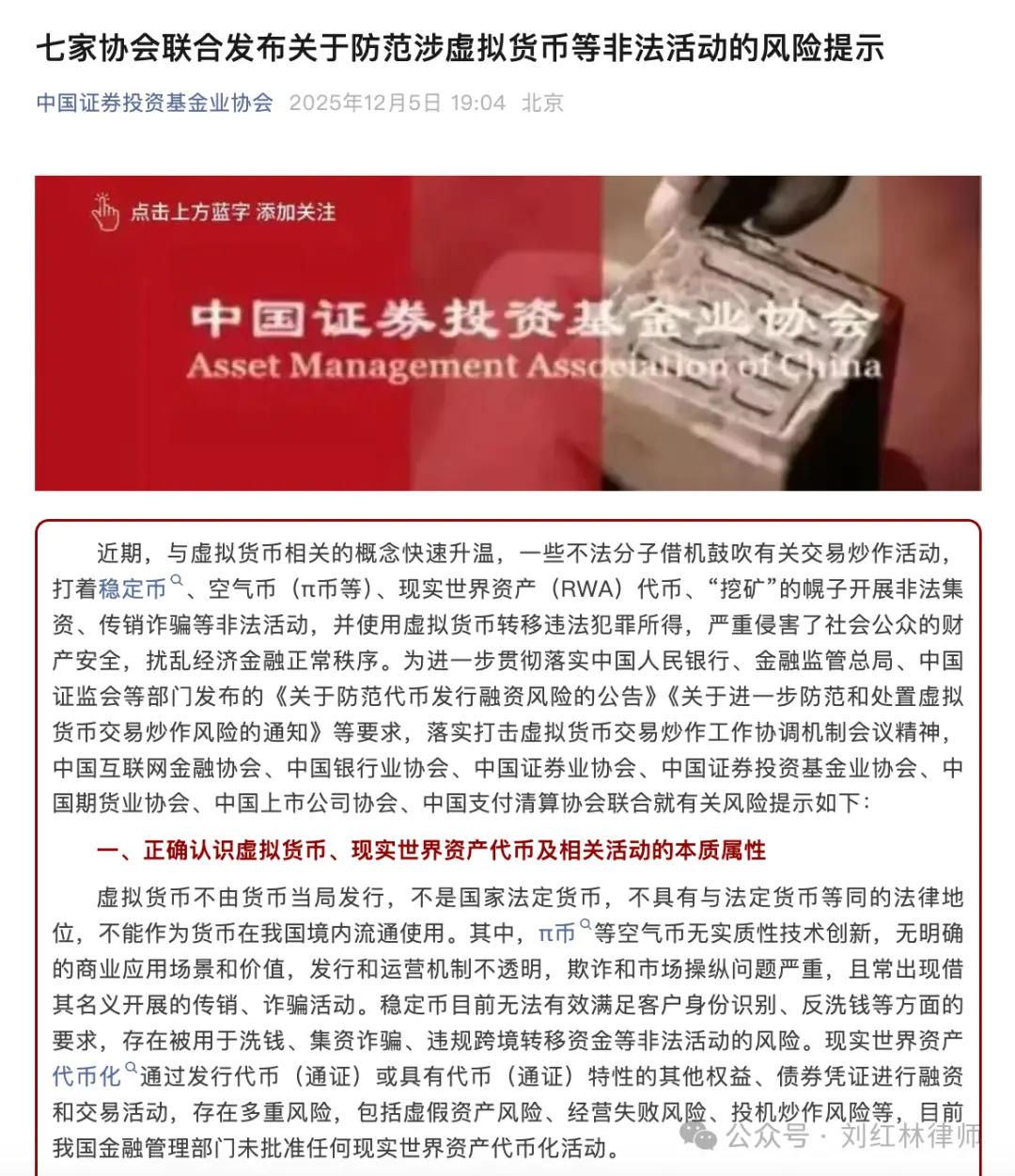

Simply now, a message all of the sudden circulated on lawyer Honglin’s WeChat Moments: a joint danger warning issued by seven financial {industry} associations concerning the prevention of illegal actions involving digital currencies. The China Web Finance Affiliation, China Banking Affiliation, China Securities Affiliation, China Asset Administration Affiliation, China Futures Affiliation, China Affiliation of Listed Firms, and China Fee and Clearing Affiliation all signed the warning.

After studying the doc, Lawyer Honglin was fully bewildered.

This is no atypical assertion from an {industry} affiliation; it is a blatant cross-industry, cross-regulatory “unified messaging” operation. Related affiliation collaborations usually happen at essential junctures in the prevention and management of systemic financial dangers.

One can not help however surprise, might RWA actually be that harmful?

Essentially the most notable facet of this doc is its first express point out of RWA (Actual-World Asset Tokenization), together with a qualitative evaluation. All through the doc, RWA is listed alongside stablecoins, nugatory cryptocurrencies, and cryptocurrency mining as a main manifestation of “illegal actions associated to digital currencies,” successfully drawing criticism from the outset.

This wording itself sends a robust sign: RWA is now not a “new know-how” awaiting regulatory clarification, however a “dangerous enterprise” immediately included in the regulatory crackdown record.

Particularly, the doc describes RWA as follows: “Actual-world asset tokenization entails financing and buying and selling actions by way of the issuance of tokens or different rights and debt devices with token traits. This carries a number of dangers, together with the danger of fictitious property, the danger of enterprise failure, and the danger of hypothesis. At the moment, my nation’s financial regulatory authorities haven’t permitted any real-world asset tokenization actions.”

This assertion clearly outlines three backside strains:

First, RWA is explicitly outlined as a “financing and buying and selling exercise.” Because of this regardless of whether or not it is backed by real-world property or makes use of blockchain know-how, it is basically a fundraising mechanism. So long as it entails token issuance, asset buying and selling, and revenue distribution, it naturally falls below the regulatory scope of the current financial authorized framework, particularly the areas prohibited by related legal guidelines similar to the Securities Regulation and the Measures for the Prohibition of Illegal Financial Establishments and Illegal Financial Enterprise Actions.

Second, regulators emphasize the dangers of “pretend property,” “enterprise failure,” and “speculative manipulation.” This is not solely a characterization of fraudulent tasks but additionally a denial of the potential market dangers of so-called “regular tasks.” Even when the challenge crew believes that its property are real, its know-how is clear, and its construction is compliant, the regulator’s judgment stays: such a token construction can not assure the authorized possession and liquidation capabilities of the underlying property, and the extent of its danger spillover is uncontrollable.

Third, and extra crucially, is the assertion: “my nation’s financial regulatory authorities haven’t permitted any real-world asset tokenization actions.” This is tantamount to a direct declaration that every one tokenized property, companies, matching platforms, and buying and selling platforms at present working below the identify RWA lack a authorized foundation for operation. There is no room for clarification that it is “in the regulatory exploration stage,” nor is there any chance of it “awaiting registration.”

In truth, RWA has been considered an “different token path” inside the {industry} for a while. Particularly after stablecoins have been formally included in the cryptocurrency regulatory framework, many groups selected to show to RWA, trying to avoid laws through the use of phrases similar to “real-world asset anchoring,” “abroad compliance path,” and “know-how service output.” This doc has refuted these claims one after the other.

The doc explicitly states that RWA’s actions pose authorized dangers similar to “illegal fundraising, unauthorized public providing of securities, and illegal operation of futures enterprise.” These statements aren’t generalities however slightly direct characterizations primarily based on express provisions in the Felony Regulation and the Securities Regulation.

- Should you situation RWA tokens to the basic public and lift funds, you’re suspected of illegal fundraising.

- Should you facilitate transactions or distribute tokens with out permission, it’s possible you’ll be committing an illegal securities providing.

- In case your token buying and selling entails leverage or betting mechanisms, it might represent illegal operation of a futures enterprise.

These fees are already very clear in phrases of authorized utility, and lately, many courtroom judgments have been made primarily based on comparable logic. RWA is not a new species current outdoors the regulation, however slightly a “acquainted goal” that regulators have categorized as half of the current financial enforcement toolbox.

The timing of this danger warning is intently associated to the frequent prevalence of fraudulent actions working below the “RWA identify” in latest instances. Beforehand, lawyer Hong Lin was invited to take part in a program on Shanghai Folks’s Radio, the matter of which was “Stopping RWA Financial Scams.” Unexpectedly, this matter has risen to the nationwide stage.

The primary paragraph of the doc from the seven associations mentions that “criminals are taking benefit of this to advertise associated buying and selling and hypothesis actions, utilizing stablecoins, nugatory cash (similar to π coin), Actual-World Asset (RWA) tokens, and ‘mining’ as a guise to hold out illegal fundraising, pyramid schemes, and different illegal actions.” Plainly regulatory authorities are judging RWA on the identical stage as nugatory cash, pyramid schemes, and different high-risk fraudulent strategies, reflecting the precise frequency of instances and social hurt noticed by regulation enforcement.

Extra importantly, this discover particularly emphasizes the joint legal responsibility of service suppliers and intermediaries. The unique textual content states: “Home employees of related abroad digital foreign money and real-world asset token service suppliers, in addition to home establishments and people who knowingly or ought to have identified that they’re engaged in digital currency-related companies and nonetheless present companies to them, shall be held accountable in accordance with regulation.”

This assertion has a profound impact and deserves our particular consideration.

First, it targets not solely challenge house owners but additionally service suppliers inside the ecosystem, together with challenge planners, know-how outsourcing suppliers, advertising brokers, KOL promoters, and cost interface suppliers. Second, “understanding or ought to have identified” is a authorized presumption of legal responsibility, now not restricted to subjective intent; so long as there is a affordable goal foundation for judgment, legal responsibility will be established. Third, it explicitly negates the frequent “abroad entity + home personnel” working mannequin in the Web3 {industry}. Even when your organization is registered abroad however your crew operates in mainland China, you can not escape the classification of “offering companies inside China.”

In different phrases, there is no such factor as “pure know-how corporations are nice” or “I am simply offering infrastructure” that absolves you of legal responsibility. If you realize this challenge is implementing RWA in mainland China and nonetheless select to supply companies, you possibly can be held accountable.

This additionally implies that the complete Web3 service chain constructed round RWA has virtually fully ceased inside China. Not solely are tasks now not viable, however the supporting companies additionally lack a viable enterprise mannequin. Groups eager to develop RWA in the future have just one choice: to “go fully abroad.” From authorized construction, asset custody, consumer entry, compliance auditing, and financial companies, each hyperlink should be indifferent from the Chinese language market, with no remaining foothold or connection. In any other case, even merely hiring an operations individual in China might set off authorized dangers.

At the moment, many tasks are nonetheless trying to safe coverage house for RWA from the perspective of “technological innovation.” They emphasize the effectivity of on-chain clearing, the transparency of asset transfers, or suggest “technical options” similar to integrating KYC and constructing multi-layered audit buildings. Nonetheless, the sign launched by regulators this time is very clear: it isn’t a technical situation, nor a mechanism situation, however slightly that the real-world financial dangers far outweigh these technological advantages. Your entire danger warning doc incorporates no phrases like “know-how pilot,” “categorized regulation,” or “prudent growth,” indicating that the regulatory objective is to not optimize the operation of RWA, however to explicitly exclude it from authorized boundaries.

This is not simply a tightening of coverage; it is a full rejection of the underlying path. It ends the very basis of the RWA mannequin—regardless of whether or not you distribute tokens utilizing an SPV structure or handle underlying fairness with on-chain contracts, so long as the closing construction possesses the attributes of “financing + buying and selling,” it can not escape the regulatory definition of illegal financial exercise. Initiatives nonetheless increasing their market on WeChat teams, Telegram teams, and Twitter below the guise of “node companions” or “regional representatives” are now not thought-about fringe explorations from a regulatory perspective; they’re immediately categorized as taking part in illegal actions.

For groups inside China, this additionally implies that the complete narrative surrounding RWA—from asset suppliers, know-how growth, and market matchmaking to the accompanying consulting, outsourcing, and promotional companies—now not possesses any sustainable enterprise logic. So long as there are Chinese language nodes in the chain, it poses a potential danger.

For abroad tasks, the state of affairs is not significantly better. The Chinese language mainland market is now not a area “ready for regulatory clarification,” however slightly a area that has clearly expressed its rejection—not a suspension, not a wait-and-see method, not a postponement, however a clear exclusion.

On this context, the selections left to practitioners are very clear: both fully relocate their enterprise techniques to a compliance system that has no overlap with Chinese language laws, or fully abandon RWA.

{kind=link}