Key Takeaways

- Riot Platforms operates 1.86 GW of energy capability, supporting Bitcoin mining right now and AI/HPC progress forward.

- RIOT reported sturdy Q3 revenues and web earnings, aided by working leverage and energy curtailment credit.

- TeraWulf’s AI push brings lengthy-time period contracts, however heavy debt, losses and execution danger stress the inventory.

The Bitcoin mining sector is in a transition part as operators are more and more specializing in digital infrastructure and AI internet hosting to diversify revenues. TeraWulf (WULF – Free Report) and Riot Platforms (RIOT – Free Report) are publicly traded Bitcoin miners in the United States that function giant-scale services powered by low-value power. TeraWulf differentiates itself by way of a robust deal with zero-carbon power and increasing AI and excessive-efficiency computing capability by way of joint ventures, whereas Riot Platforms stands out as certainly one of the largest pure-play miners with a rising information-middle footprint.

Latest strikes, together with TeraWulf’s secured-undertaking financing tied to its Fluidstack three way partnership and Riot Platforms’ secure November BTC manufacturing and infrastructure enlargement, spotlight how every is adapting to a quickly evolving mining and computing panorama.

So, which inventory affords higher upside, TeraWulf or Riot Platforms? Let’s discover out.

The Case for WULF Stock

The corporate’s evolution from Bitcoin mining to AI and HPC infrastructure is related to a number of structural dangers and implementation challenges. Though TeraWulf maintains 245 megawatts of mining capability at Lake Mariner, revenues are nonetheless in danger as a consequence of Bitcoin worth volatility, rising community issue and halving-associated pressures. This publicity was evident as Bitcoin output steadily declined to 377 BTC in the third quarter of 2025.

HPC enlargement has materially elevated TeraWulf’s capital depth and leverage. The corporate raised greater than $5 billion in 2025 by way of convertible notes and secured debt, pushing whole debt to roughly $1.5 billion. Excessive leverage will increase refinancing and curiosity expense danger and contributes to extreme earnings volatility, together with a big GAAP loss related to a non-money revaluation in the third quarter of 2025.

WULF faces challenges from executing giant-scale information middle builds, greater working bills from AI and HPC enlargement, and continued sensitivity to Bitcoin volatility. In opposition to this backdrop, the firm’s inventory fell practically 11% to $11.57 on Wednesday as traders grew to become cautious of heavy AI spending.

Nonetheless, TeraWulf advantages from low-value, clear energy, vertically built-in website growth and lengthy-time period, credit score-enhanced HPC leases. Throughout the third quarter of 2025, the firm commenced recurring HPC lease revenues and secured over $16 billion in lengthy-time period HPC contracts, together with Fluidstack leases backed by Google, offering sturdy income visibility.

Alternatives lie in AI and hyperscale demand. Administration reaffirmed a goal of 250-500 MW of recent HPC capability contracted yearly, supported by enlargement at Lake Mariner, the Abernathy JV in Texas (as much as 600 MW), and the lengthy-dated Cayuga website lease starting in 2027.

The Zacks Consensus Estimate for the first quarter of 2026 loss is at present pegged at 18 cents per share, unchanged over the previous 30 days, barely worse than a lack of 16 cents reported a yr in the past.

Picture Supply: Zacks Funding Analysis

The Case for RIOT Stock

Riot Platforms is transitioning from a pure-play Bitcoin miner towards an information middle growth mannequin, supported by its vertically built-in operations and absolutely permitted land and energy portfolio. In the third quarter of 2025, the firm operated Texas and Kentucky mining websites with roughly 1.86 GW of energy capability, positioning it for future AI and HPC enlargement.

Key benefits for Riot Platforms embody its giant scale, low-value energy entry and monetary flexibility. In the third quarter, the firm generated $180.2 million in revenues, primarily from Bitcoin mining, and reported web earnings of $104.5 million, benefiting from sturdy working leverage and energy curtailment credit of $30.7 million.

Riot Platforms’ progress alternative lies in AI and HPC growth at the Corsicana website, the place Core & Shell building has began on two information middle buildings with 112 MW of important IT capability. The campus is deliberate to scale to 1 GW over time, and administration famous ongoing leasing talks with hyperscaler, neocloud and enterprise prospects, creating potential upside as contracts are executed.

Regardless of progress plans, the firm faces stress from roughly $214 million in close to-time period capex for the Corsicana buildout and ongoing Bitcoin market volatility. These elements weighed on manufacturing, which fell 14% yr over yr to 428 in November 2025 and decreased 2% sequentially.

The Zacks Consensus Estimate for the first quarter 2026 loss is at present pegged at 20 cents per share, unchanged over the previous 30 days, representing a pointy enchancment from the 90-cent loss reported in the yr-in the past quarter.

Picture Supply: Zacks Funding Analysis

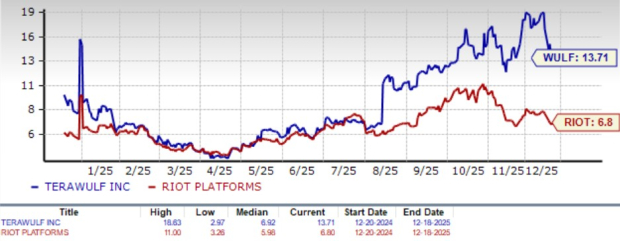

WULF vs. RIOT: Worth Efficiency & Valuation

Over the previous six months, TeraWulf shares soared 215.3%, far outpacing Riot Platforms’ 40% acquire and the Financial – Miscellaneous Services business’s 5.4% decline. Nonetheless, TeraWulf’s sharp rise comes with greater danger, together with heavy debt, ongoing losses, warrant liabilities and dear HPC enlargement that strains flexibility and raises execution danger.

In distinction, RIOT affords a extra balanced profile, with a decrease EV per accessible megawatt and an skilled in-home growth group that has accomplished greater than 200 initiatives, decreasing execution danger as its AI-targeted enlargement progresses.

Stock Efficiency

Picture Supply: Zacks Funding Analysis

Each TeraWulf and Riot Platforms’ shares are at present overvalued, as advised by a Value Score of F.

On the valuation entrance, TeraWulf trades at a ahead 12-month worth-to-gross sales (P/S) a number of of 13.71, greater than double Riot Platforms’ 6.8. TeraWulf’s greater a number of displays optimism however will increase sensitivity to execution and financing dangers, whereas Riot Platforms’ decrease valuation affords a extra conservative and interesting entry level.

P/S F12M Ratio

Picture Supply: Zacks Funding Analysis

Conclusion

Whereas TeraWulf affords sturdy AI and HPC progress potential, its premium valuation, greater leverage and execution danger from capital-intensive enlargement make the inventory riskier. Riot Platforms stands out with higher scale, decrease EV per megawatt, steadier money era from Bitcoin mining and a confirmed in-home growth monitor document. With stronger monetary flexibility to fund AI enlargement and a extra conservative valuation, Riot Platforms supplies extra sturdy upside and emerges as the higher funding selection.

RIOT at present carries a Zacks Rank #3 (Maintain), whereas WULF has a Zacks Rank #4 (Promote).

You may see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

{kind=link}