The Individuals’s Financial institution of China and 7 different ministries and commissions collectively issued regulatory provisions associated to digital currencies and real-world asset (RWA) tokenization: Discover of the Individuals’s Financial institution of China, Nationwide Improvement and Reform Fee, Ministry of Business and Data Expertise, Ministry of Public Safety, State Administration for Market Regulation, Nationwide Monetary Regulatory Administration, China Securities Regulatory Fee, and State Administration of Overseas Alternate on Additional Stopping and Disposing of Dangers Associated to Digital Currencies and Different Actions (Yin Fa [2026] No. 42) (hereinafter known as “Doc No. 42”).

Beforehand, rumors had circulated inside the trade concerning the impending new laws. After the official doc was launched, its content material was discovered to be complete. After studying it, ShaLv felt that the earlier compliance explorations within the RWA subject had been virtually completely addressed within the paperwork issued by the eight departments and the CSRC.

Let’s take a fast learn:

1. The Nature of Doc No. 42

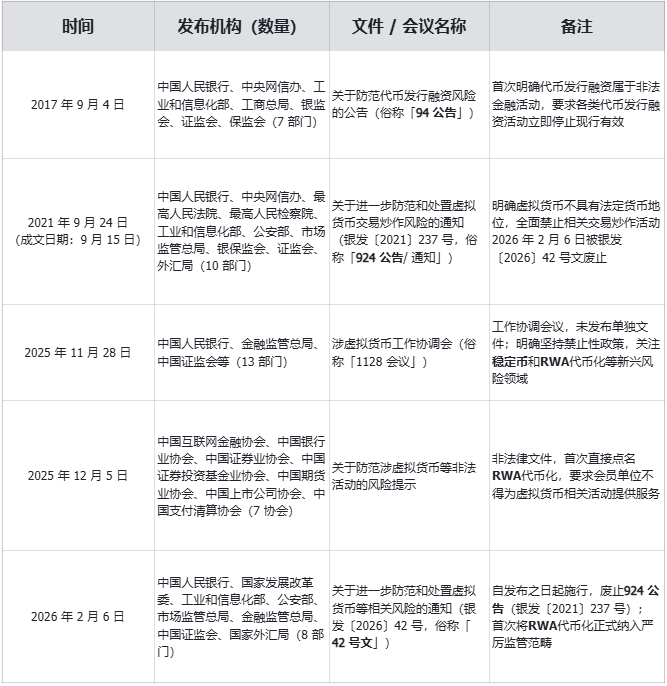

In 2017 and 2021, regulators successively issued the “94 Announcement” and the “924 Announcement.” Since then, there was an extended interval with out the introduction of a whole authorized doc on this subject. The inter-ministerial coordination assembly of 13 departments on the finish of 2025 and the danger warnings issued by seven associations don’t represent formal upgrades to authorized paperwork. The next is a comparability of the character of 5 core associated paperwork:

(*8*)

Core Conclusion: Doc No. 42 is at the moment probably the most exact and complete authorized normative doc within the subject of digital currency-related enterprise. The “924 Announcement” has been formally repealed upon its implementation.

2. Core Variations Between Doc No. 42 and Earlier Digital Foreign money Regulatory Paperwork

(1) Complete Growth of Regulatory Scope

- Addition of Core Regulatory Targets: For the primary time, real-world asset tokenization (RWA) and stablecoins have been included as core regulatory targets. The regulatory dimension has expanded from mere digital forex buying and selling and hypothesis to a trinity of “digital forex + RWA + stablecoins,” enabling full-chain supervision.

- Refined Stablecoin Regulation: Clearly states that “stablecoins pegged to fiat forex partially carry out the features of fiat forex in circulation and use.” Prohibits “any home or international entity or particular person from issuing stablecoins pegged to the RMB abroad with out the lawful and regulatory approval of related departments.”

- Clear Definition of RWA: Defines it as “actions that use encryption expertise and distributed ledger or related expertise to transform asset possession, earnings rights, and so on., into tokens or different fairness or debt certificates with token traits, and conduct issuance and buying and selling actions.”

(2) Elevated Issuing Authority and Authorized Impact

Doc No. 42 was collectively issued by eight departments together with the PBOC and the NDRC. It additionally reached consensus with three different departments: the Our on-line world Administration of China, the Supreme Individuals’s Courtroom, and the Supreme Individuals’s Procuratorate, and was authorised by the State Council. Its issuing stage and authorized impact are considerably larger than earlier paperwork.

(3) Up to date and Improved Authorized Foundation

Provides higher-level authorized bases such because the “Futures and Derivatives Legislation of the Individuals’s Republic of China,” the “Securities Funding Fund Legislation of the Individuals’s Republic of China,” and the “Regulations of the Individuals’s Republic of China on the Administration of the Renminbi,” offering extra complete authorized help. Concurrently, removes some paperwork referenced within the 924 Announcement, such because the “Regulations on the Administration of Futures Buying and selling” and the “State Council Choice on Rectifying Varied Buying and selling Venues to Successfully Forestall Monetary Dangers,” making authorized software extra exact.

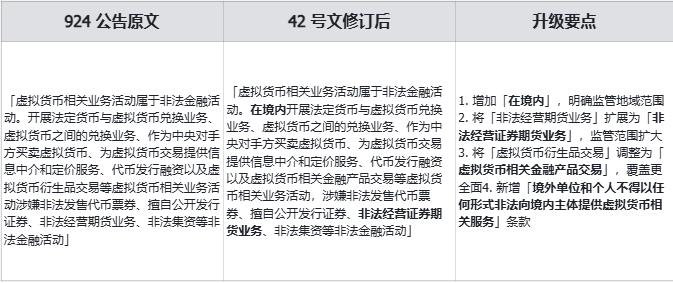

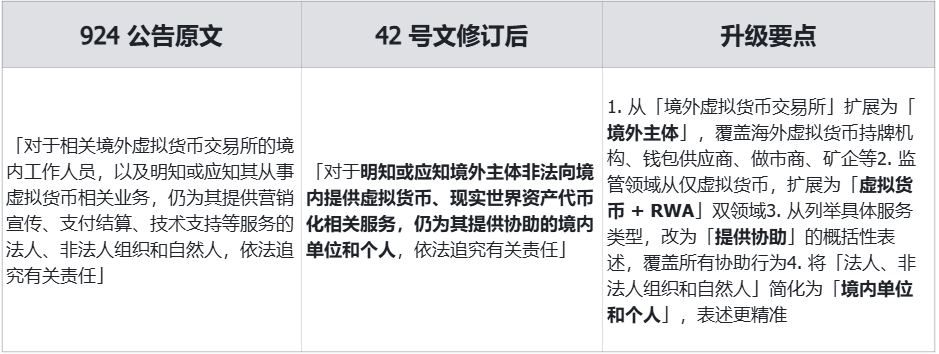

(4) Exact Improve within the Characterization of Digital Currencies

(*8*)

(5) New Definitions for RWA and Stablecoins

Doc No. 42 provides particular clauses defining the character of RWA: “Inside China, conducting real-world asset tokenization actions, in addition to offering associated middleman and knowledge expertise providers, and so on., are suspected of unlawful monetary actions comparable to unlawful issuance of token vouchers, unauthorized public providing of securities, unlawful operation of securities and futures enterprise, and unlawful fundraising, and shall be prohibited; aside from associated enterprise actions carried out counting on particular monetary infrastructure with the lawful and regulatory approval of the competent enterprise authorities.”

Concurrently clarifies the ban on RWA providers from abroad: “Abroad entities and people shall not present real-world asset tokenization-related providers to home entities in any type illegally.”

Core Conclusion: Primarily based on the above clauses, it’s clear that:

1. RWA challenge situated in China, service supplier in China — Unlawful

2. RWA challenge situated in China, service supplier abroad — Unlawful

3. NFT initiatives of the same nature, suspected of unlawful issuance of token vouchers — Unlawful

4. RWA challenge situated abroad, suspected of unlawful fundraising inside China — Unlawful

(6) Refined Division of Regulatory Tasks, from Multi-department Coordination to Twin-track Supervision

The 924 Announcement solely established a multi-department coordination mechanism: “The Individuals’s Financial institution of China, along with the Our on-line world Administration of China, the Supreme Individuals’s Courtroom, the Supreme Individuals’s Procuratorate, the Ministry of Business and Data Expertise, the Ministry of Public Safety, the State Administration for Market Regulation, the China Banking and Insurance coverage Regulatory Fee, the China Securities Regulatory Fee, and the State Administration of Overseas Alternate, shall set up a piece coordination mechanism.”

Doc No. 42 innovatively implements a dual-lead system, clearly dividing regulatory duties into two strains:

1. Digital Foreign money Regulation: “The Individuals’s Financial institution of China, along with the Nationwide Improvement and Reform Fee, the Ministry of Business and Data Expertise, the Ministry of Public Safety, the State Administration for Market Regulation, the Nationwide Monetary Regulatory Administration, the China Securities Regulatory Fee, the State Administration of Overseas Alternate, and different departments, shall enhance the work mechanism.”

2. RWA Regulation: “The China Securities Regulatory Fee, along with the Nationwide Improvement and Reform Fee, the Ministry of Business and Data Expertise, the Ministry of Public Safety, the Individuals’s Financial institution of China, the State Administration for Market Regulation, the Nationwide Monetary Regulatory Administration, the State Administration of Overseas Alternate, and different departments, shall enhance the work mechanism.”

Core Conclusion:

1. The earlier downside of ineffective multi-department coordination is addressed, because the clear higher-level legal guidelines and accountability mechanisms depart no room for buck-passing or negligence.

2. Market entities desiring to discover associated companies can clearly perceive the federal government’s energy record and scope of duties, decreasing enterprise misjudgments.

(7) Strengthened Native Departmental Accountability

Constructing upon the 924 Announcement, Doc No. 42 provides: “Particularly led by native monetary administration departments, with participation from branches and dispatched workplaces of the State Council’s monetary administration departments, in addition to telecommunications authorities, public safety, market regulation, and different departments, coordinating with our on-line world departments, individuals’s courts, and other people’s procuratorates.” This clarifies the lead division and collaboration mechanism on the native implementation stage, additional solidifying native regulatory duty.

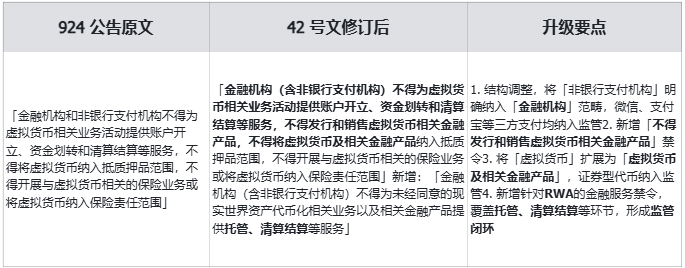

(8) Strengthened Administration of Monetary Establishments

(9) Expanded Regulation of Middleman and Expertise Service Suppliers

The regulatory scope of the 924 Announcement was restricted to digital currency-related providers. Doc No. 42 provides: “Related middleman establishments and knowledge expertise service establishments shall not present middleman, technical, or different providers for real-world asset tokenization-related companies and associated monetary merchandise that haven’t been authorised,” formally extending the regulatory scope to middleman and expertise service suppliers within the RWA subject.

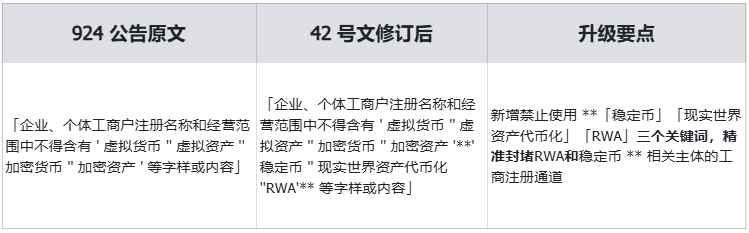

(10) Tightened Registration and Administration of Market Entities

(11) Enhanced Crackdown on Mining

The 924 Announcement solely talked about “attaining full-chain monitoring and full-time data backup for digital forex ‘mining,’ buying and selling, and alternate.” Doc No. 42 individually lists Article 9 with detailed provisions, clearly stating “strictly prohibit ‘mining machine’ producers from offering providers comparable to ‘mining machine’ gross sales inside China,” chopping off the mining trade chain at its supply. In comparison with the monitoring necessities of the 924 Announcement, the brand new laws are stricter, extra enforceable, and make clear the dealing with mechanisms for related departments after receiving leads.

(12) Modern Regulation of Abroad Issuance

Doc No. 42, contemplating new developments within the abroad crypto subject, provides twin prohibitions on abroad issuance for cross-border enterprise:

1. With out lawful and regulatory approval from related departments, home entities and their managed abroad entities shall not problem digital currencies abroad.

2. Relating to RWA: “Home entities instantly or not directly going abroad to conduct real-world asset tokenization enterprise within the type of exterior debt, or conducting asset-backed securitization-like or equity-like real-world asset tokenization enterprise abroad primarily based on home asset possession, earnings rights, and so on., shall be strictly supervised by related departments such because the Nationwide Improvement and Reform Fee, the China Securities Regulatory Fee, and the State Administration of Overseas Alternate based on their respective duties and in accordance with legal guidelines and laws, following the precept of ‘similar enterprise, similar danger, similar guidelines.'”

Core Conclusion: Primarily based on the above clauses, it’s clear that:

1. Abroad token issuance of the non-RWA sort with out underlying belongings — Unlawful

2. Safety tokenization conduct just like exterior debt, fairness, or ABS — Authorized below strict supervision

3. Regulatory precept for authorized RWA — Check with securities enterprise: “similar enterprise, similar danger, similar guidelines”

(13) Strengthened Supervision and Accountability for Abroad Enterprise of Home Monetary Establishments

Doc No. 42 provides: “Abroad subsidiaries and branches of home monetary establishments offering real-world asset tokenization-related providers abroad shall act lawfully, prudently, and steadily, outfitted with skilled personnel and programs, successfully forestall enterprise dangers, strictly implement necessities comparable to buyer due diligence, suitability administration, and anti-money laundering, and incorporate them into the compliance and danger management administration system of the home monetary establishment,” attaining a look-through supervision of cross-border enterprise.

Core Conclusion: Primarily based on the above clauses, it’s clear that:

1. Abroad branches of home monetary establishments (subsidiaries, branches, and so on.) can conduct tokenization-related enterprise.

2. Abroad branches conducting tokenization enterprise should adjust to each native legal guidelines and Chinese language regulatory necessities, fulfilling extremely prudent, anti-money laundering, and different authorized obligations.

3. Enterprise data and information of abroad branches have to be absolutely integrated into the compliance and danger management system of the home monetary establishment.

(14) Regulatory Protection of Cross-border Companies by Middleman Establishments

Doc No. 42 provides: “Middleman establishments and knowledge expertise service establishments that present providers for home entities instantly or not directly going abroad to conduct real-world asset tokenization enterprise within the type of exterior debt, or conducting real-world asset tokenization-related enterprise abroad primarily based on home rights and pursuits, shall strictly adjust to legal guidelines and laws, and in accordance with related normative necessities, set up and enhance related compliance and inner management programs, strengthen enterprise and danger administration and management, and report or file the related enterprise improvement state of affairs with related administration departments for approval or submitting,” formally bringing cross-border service middleman establishments into the regulatory scope.

Core Conclusion: Primarily based on the above clauses, it’s clear that:

1. Middleman establishments comparable to regulation companies and expertise firms can present tokenization-related providers inside a managed regulatory scope.

2. Middleman establishments conducting tokenization enterprise should have sound danger management and inner management programs, and their enterprise improvement have to be reported or filed with regulatory departments for approval or submitting.

(15) Expanded Scope of Authorized Legal responsibility Topics

(16) Optimized Civil Legal responsibility Clauses

The 924 Announcement stipulated: “Any authorized individual, unincorporated group, or pure individual investing in digital currencies and associated derivatives, if it violates public order and good customs, the associated civil authorized act is invalid.” Doc No. 42 revises this to: “Any entity or particular person investing in digital currencies, real-world asset tokens, and associated monetary merchandise, if it violates public order and good customs, the associated civil authorized act is invalid,” increasing the funding targets from “digital currencies and associated derivatives” to “digital currencies, real-world asset tokens, and associated monetary merchandise,” attaining extra complete regulatory protection.

Core Conclusion: Varied pyramid schemes soliciting funds from home buyers within the title of RWA is not going to have their funding rights and pursuits protected by regulation.

3. Present Standing and Future Path of RWA Enterprise

The idea and initiatives of RWA first emerged abroad, just like the early STO idea however with broader creativeness, dubbed “all the pieces could be RWA” inside the trade. Home discussions about RWA steadily heated up beginning in 2024, reaching a peak in quantity from June to August 2025. This pattern is carefully associated to the entry of main home establishments like Ant Group, JD.com, and Guotai Junan, in addition to the upgrading of crypto regulation, the introduction of stablecoin laws, and the continual issuance of licenses in areas like the US and Hong Kong.

Present Mainstream RWA Tasks and Underlying Belongings

1. Rising working money movement belongings comparable to new vitality and computing energy

2. Conventional working belongings comparable to business leases

3. Shopper items initiatives for cultural IP value-added

4. Bodily belongings comparable to actual property, antiques, artworks, and minerals

5. Different forms of belongings

Mainstream RWA Financing Options for Practitioners

1. In international locations and areas with clear regulatory provisions, conduct safety token choices (STOs) for the above-mentioned varieties 1 and a pair of belongings — utterly authorized, however with the very best regulatory necessities and operational prices.

2. Problem on home platforms comparable to cultural asset exchanges, digital asset exchanges, and property rights exchanges for the above-mentioned sort 3 belongings and NFTs — decrease regulatory necessities, not explicitly outlined as unlawful.

3. Problem token initiatives missing money movement help for the above-mentioned varieties 4 and 5 belongings on abroad centralized and decentralized exchanges — seemingly have underlying belongings, however are literally high-risk behaviors involving recruitment, hypothesis, fundraising, and market manipulation, not but exactly outlined in authorized texts.

Because of vital variations in underlying asset traits, fundraising targets, operational standardization, and challenge crew values, there are quite a few gray-area operations within the RWA subject. Practitioners additionally interact in behaviors that intentionally blur regulatory boundaries. With out strict supervision, it’s simple for dangerous cash to drive out good, resulting in frequent high-risk initiatives and mass fraud incidents. At present, individuals on this subject are combined, together with home and international securities establishments, issuance service suppliers, abroad exchanges, digital compradors, information service suppliers, and home property rights exchanges.

Nonetheless, with the introduction of Doc No. 42, all the pieces has modified. By way of meticulous evaluation, the regulators’ pondering and philosophy could be discerned:

1. Legislators comprehensively thought of legal guidelines and laws from areas comparable to the US, Europe, and Hong Kong, referencing them in regulatory hyperlinks and expressions, attaining reasonable alignment with worldwide regulation.

2. The brand new laws comprehensively cowl rising fields comparable to stablecoins and RWA, whereas filling earlier regulatory grey areas like mining machine gross sales and mining regulation enforcement.

3. In areas the place technological maturity is inadequate and rule-making energy

{kind=link}