Posted April 3, 2024 at 1:25 pm EST.

A major dialogue to reevaluate Ethereum’s token issuance mannequin has stirred debate over the way forward for ETH staking economics.

As Ethereum sees an upward development in ETH staking, projections counsel this might lead to a majority of ETH being locked in staking contracts, prompting considerations over the community’s future dynamics. In response, Ethereum Basis researchers Ansgar Dietrichs and Caspar Schwarz-Schilling have launched a proposal to tweak Ethereum’s issuance coverage to preserve a balanced staking ratio, aiming to forestall potential detrimental results similar to inflationary pressures on non-stakers and centralization dangers.

Nevertheless, this answer has sparked a contentious debate inside the Ethereum group, with some members voicing robust opposition in opposition to altering the financial coverage in a approach they imagine might undermine Ethereum’s foundational rules and its attraction to institutional traders.

As James Spediacci tweeted, “It nearly looks like a coordinated assault on Ethereum that a few individuals are suggesting adjusting the ETH issuance curve once more and altering the financial coverage when the SEC at the moment has Ethereum underneath a microscope.”

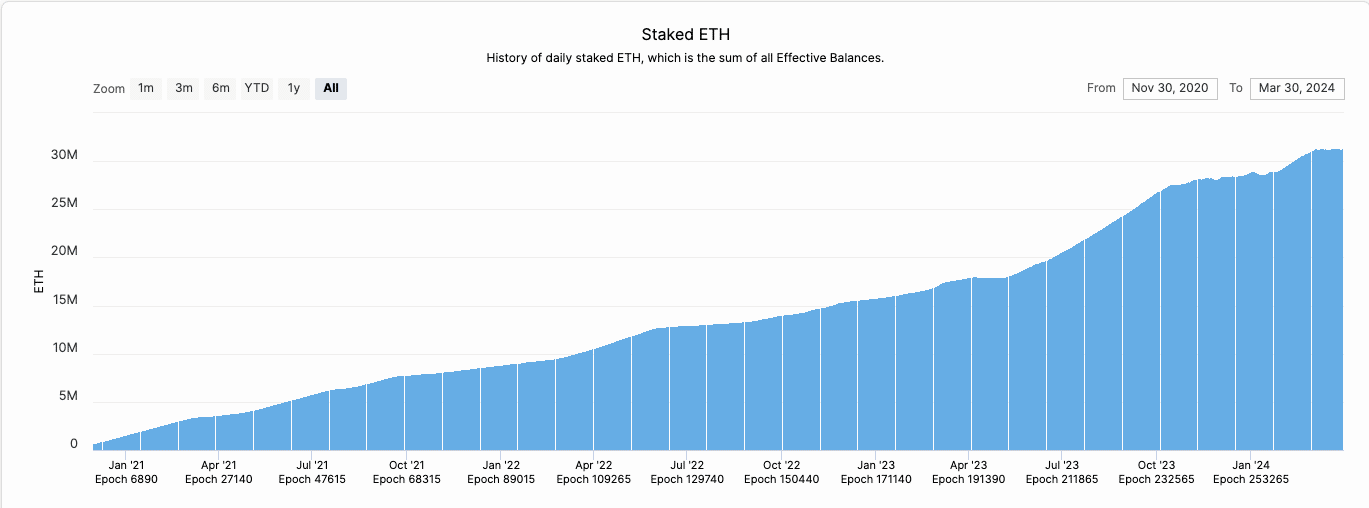

The Quantity of Staked ETH Has Been on the Rise

Since Ethereum’s transition from Proof of Work to Proof of Stake 18 months in the past, often known as “The Merge,” the dynamics of ETH staking have shifted dramatically. Presently, about 31 million ETH, roughly 26% of the whole provide, are staked. This determine has been on an upward trajectory, from 11% at the time of the Merge and 15% at the time of the Shapella improve, which enabled the withdrawal of staked ETH from the Beacon Chain in April 2023.

There are a number of drivers behind the progressive improve in staking, together with the general enchancment in the community’s safety and stability, improvements like liquid staking suppliers that decrease the barrier to entry for staking, and the enticement of further rewards. Notably, these further rewards embrace these from Maximal Extractable Worth (MEV), in addition to alternatives for airdrop farming, which add to the attractiveness of staking past the main consensus layer rewards.

Staking Demand Will Proceed to Enhance

The staking ratio is ready to improve in the upcoming months and years, as highlighted in a weblog post by Mike Neuder from the Ethereum Basis, due to 5 causes:

- Appreciating ETH Worth: An rising ETH worth makes staking extra enticing due to larger USD-denominated yields.

- Restaking Demand: Platforms like EigenLayer are driving curiosity in restaked ETH, with the potential for airdrops including to the attraction.

- Curiosity Charges: Decrease rates of interest might shift institutional capital in the direction of staking for higher yields.

- Liquid Staking Tokens (LST)/Liquid Restaking Tokens (LRT): These tokens decrease the barrier to staking and are anticipated to appeal to vital capital inflows.

- Staked ETH ETFs: The potential of Ethereum-based ETFs, which embrace staking in their mannequin, might introduce a substantial new viewers to staking.

Why a Excessive Staking Ratio Would possibly Be Dangerous

Nevertheless, the prospect of a frequently rising staking ratio raises a number of considerations.

“We argue that top staking ratio regimes include detrimental externalities that have an effect on ETH holders, (solo) stakers, in addition to the protocol itself,” they wrote in the proposal.

Dietrichs and Schwarz-Schilling’s evaluation factors out potential points with almost all ETH being staked, notably with a good portion being locked in LSTs similar to Lido’s stETH, Coinbase’s cbETH, or Rocket Pool’s rETH. In accordance to the authors, a state of affairs the place the staking ratio approaches 100% is troubling for a number of causes:

- Actual staking yield will diminish: As the staking price approaches 100%, actual yields from staking might drop to zero. Though rewards from the protocol proceed, the whole provide of ETH will increase at the identical price, successfully nullifying actual positive aspects for stakers.

- ETH will develop into “costly” cash: Excessive staking charges might make holding ETH expensive due to elevated inflationary strain on non-stakers. When numerous ETH is staked, individuals who don’t stake see the quantity of their ETH lower proportionally in contrast to those that do stake. This might undermine ETH’s position as a cost-effective and trustless asset on the Ethereum community.

- Risk to ETH’s standing as default foreign money: The costly nature of holding ETH may problem its place as the default foreign money of Ethereum, main to friction in transactions and a shift in the direction of various tokens or protocols. Individuals may begin utilizing different tokens that give them rewards, like Lido’s stETH, for each day use. This implies ETH won’t be the major foreign money folks use on Ethereum anymore.

- Threat of centralization and “too huge to fail” entities: A couple of dominant staking tokens like Lido, which at the moment has 30% of all staked ETH, might amass extreme affect over Ethereum’s underlying protocol, posing dangers to the community’s decentralization and governance. So, if there’s a good contract vulnerability in Lido’s value, and so they symbolize the majority of the community, in idea, they may fork the chain to keep away from their losses.

The Proposal

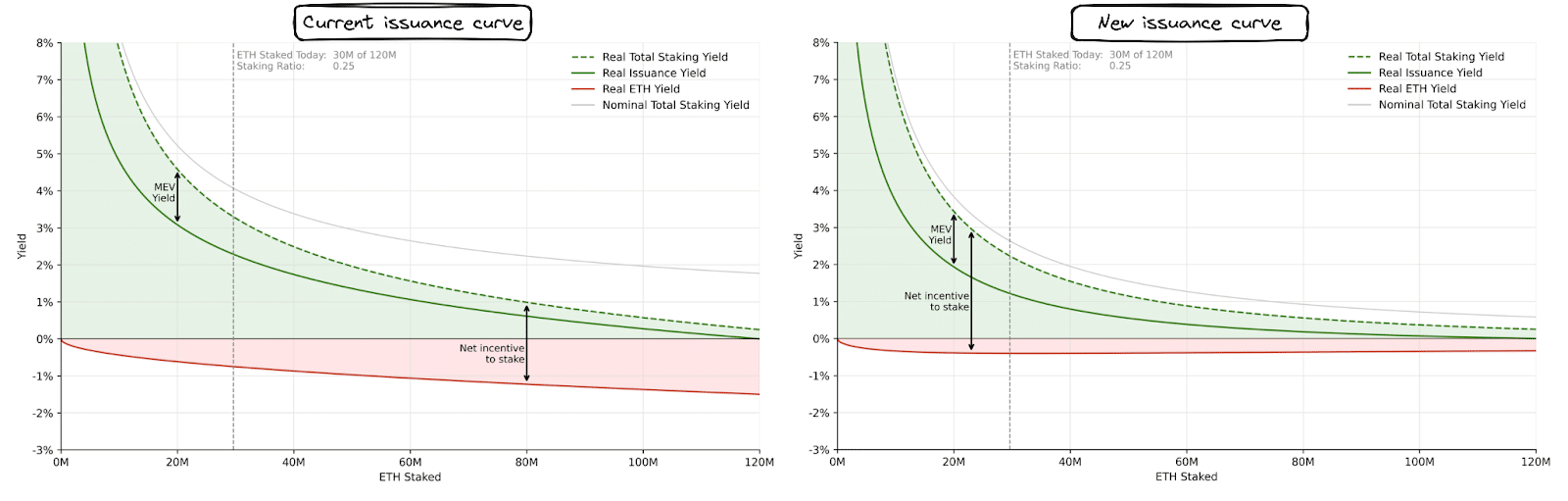

To mitigate these dangers, on February 21, Ansgar and Caspar proposed a recalibration of Ethereum’s issuance curve, which includes a shift in the direction of Stake Ratio Focusing on, a nuanced method that goals for a balanced staking ratio as a substitute of a mounted amount of staked ETH.

The proposed change goals to lower the incentive for brand new staking inflows by introducing a revised method for calculating staking rewards. The present issuance curve, outlined by a parameterized inverse sq. root perform, doesn’t cap rewards in a approach that stops an extreme whole staking ratio.

The brand new method intends to tackle this by adjusting rewards to discourage staking past a sure threshold, thus aiming to stabilize the staking ratio and guarantee community safety with out inviting detrimental externalities. Whereas the curve won’t want to flip detrimental abruptly to be efficient, a gradual method in the direction of zero rewards previous a sure staking stage might suffice to goal a appropriate staking vary. For instance, underneath the present issuance curve, at 80 million ETH staked, the nominal yield can be 2%, whereas underneath a potential revised curve, the identical quantity of ETH staked might yield 1%.

However, the authors don’t explicitly say what the splendid staking ratio ought to be. “It’s inherently arduous to objectively purpose about it and wishes to be mentioned extra broadly in the group,” they wrote.

Dietrichs and Schwarz-Schilling’s proposal, premised on the assumptions that the majority ETH will finally be staked, predominantly by way of Liquid Staking Tokens (LSTs) and Liquid Restaking Tokens (LRTs), is essentially about steering the community in the direction of an inevitable future underneath managed phrases. They argue that as staking turns into more and more prevalent, the staking rewards will naturally diminish underneath the present issuance curve.

By proposing a change in the issuance curve now, whereas the staking ratio remains to be comparatively low, they intention to alter the incentives in a approach that preempts the potential detrimental outcomes of an excessively excessive staking ratio. This proactive method seeks to preserve the stability and well being of the Ethereum ecosystem by making certain that the transition in the direction of larger staking ratios doesn’t compromise the community’s safety, dilute ETH holders unnecessarily, or drawback solo stakers.

Damaging Community Response

Whereas the Ethereum Basis researchers supposed to provoke a dialogue, the group was up in arms, with the majority signaling that this was not a good concept for Ethereum to pursue.

Eric.eth, a co-author of one in every of Ethereum’s most vital enchancment proposals (EIP-1559), is in opposition to altering the curve. “Seeing some rising dialogue from researchers and others in the group about tweaking the PoS issuance curve. The final disregard for a way arduous we’ve labored for a decade establishing ETH being cash is regarding. I’ll battle this concept with something I’ve,” he wrote on X.

His feedback echo some critics who say that frequent adjustments in financial coverage erode confidence amongst customers and traders, distancing Ethereum from the “arduous cash” attribute and “credible neutrality” that underpin its worth proposition, in distinction to the perceived stability of Bitcoin.

Gnosis co-founder Martin Köppelmann pointed out that altering the issuance curve “doesn’t essentially enhance Ethereum – it simply shifts incentives from one group to one other,” whereas Jon Charbonneau, founding father of DBA, said that “these tweaks attempt to clear up an unsolvable drawback of basic tradeoffs in PoS.”

Moreover, altering the issuance curve might dilute Ethereum’s attractiveness as a yield-generating asset for ETFs and institutional traders whose curiosity in Ethereum is predicated on its present “yield” narrative. Equally, tasks constructed on Ethereum may endure due to the shift in expectations round financial coverage stability.

Regulatory Dangers?

One other group member identified that, in the midst of the Securities and Exchange Commission investigation of the EF, this transfer will not be good, as it will indicate that the Basis certainly runs managerial efforts over Ethereum. That is vital as a result of it’s one in every of the prongs of the Howey Test, and the SEC might use it to argue that ETH is a safety.

I like and respect EF researchers.

We’d not be the place we’re with out their valuable work and so they’ll carry on being very invaluable.

However goddamnit, typically, they cannot learn the room! pic.twitter.com/Lcau6VWpAE

— Jrag.eth (@JimmyRagosa) April 1, 2024

Debate to Proceed?

Researcher Emmanuel Awoski criticized those that wouldn’t even interact in a dialog about the issuance curve. He wrote, “At present is a good day to begin calling out the development of anti-intellectualism that’s slowly permeating the discourse round the issuance curve change. Not solely are memes like this distasteful, in addition they symbolize how low we’ve fallen as a group. Now, EF researchers are getting mocked by individuals who haven’t spent their days/nights obsessing about fixing arduous issues. Individuals whose sole contribution to crypto has been ‘I’ll pour cash into some protocol and watch for the numbers to go up’.”

However detrimental sentiment has thus far appeared to prevail. Ryan Berckmans countered saying that “it’s not anti intellectualism to level out (in meme kind or in any other case) that for all its laudable technical rigor, the issuance modification proposal fails to reveal an understanding of fundamental key aspects of the change administration surroundings.”

Replace, Monday, April 3, 04:15 pm ET: An earlier model of this text mistakenly displayed the title of Caspar Schwarz-Schilling as Caspar Schwarz. Unchained regrets the error.

{kind=link}