On this week’s publication, Thad Pinakiewicz previews the approaching buying and selling debut of WLFI, issued by the Trump household’s World Liberty Monetary; Zack Pokorny analyzes Google’s entry into the company L1 race; and Lucas unpacks an trade group’s daring push to guard software program builders from prosecution.

From Locked to Liquid: World Liberty Token Set to Be Liberated

After a month of ready, World Liberty Monetary (WLFI) token holders will see the token grow to be tradable in spot markets at 8:00 a.m. ET on Monday, Sept. 1. WLFI holders voted with a convincing “sure” on the venture’s third governance proposal a month in the past, with 99.94% of tokens voting to make the token tradable.

The primary onchain unlock window will open by way of the Trump family-led venture’s lockbox, permitting eligible consumers to say 20% of their presale allocations whereas leaving subsequent unlocks to future governance votes. Onchain, the “lockbox” contract now custodies roughly 15 billion WLFI, 15% of the venture’s provide. That units up a close to‑time period liquidity occasion the place almost 3 billion WLFI tokens, price ~$950 million at current costs, can start buying and selling, adopted by DAO‑pushed provide selections in the weeks and months to return.

Notably, greater than 30,000 of the 85,873 wallets that held WLFI earlier than the lockbox launch have locked all their WLFI in the contract (a precondition for buying and selling).

OUR TAKE:

That is, by any measure, one of the crucial energetic and engaged tokenholder bases in crypto. Having over one‑third of holders actively onchain, updated, and interacting with WLFI sensible contracts is notable in DeFi, the place a lot of the sector suffers from torpid governance participation—dynamic protocols have typically been exploited by taxing idle holders.

Whereas the energetic person base is laudable, the massive portion of wallets depositing all their belongings into the lockbox indicators a broad-based intent to commerce. WLFI holders that purchased in the primary tranche at $0.015/token are sitting on a 20x achieve, and holders that purchased in the second tranche at $0.05/token are sitting on a ~6x achieve. Need to hedge and monetize the place shall be excessive, with some straightforward math for holders promoting a part of their 20% unlock to dollarize their whole funding principal.

Primarily based on premarket buying and selling ranges, WLFI’s absolutely diluted worth ranges from about $20 billion at $0.20 to about $42 billion at $0.42. With 20% of the lockbox’s ~15 billion WLFI steadiness eligible to be unlocked on Sept. 1, we will count on a minimal of three billion tokens to grow to be liquid. At $0.20 apiece, that’s about $592 million of float, and at $0.42 every, it’s about $1.24 billion. Framed in a different way, the primary launch is 20% of the $0.015 and $0.05 presale tranches, representing at most 5% of whole provide—the form of token Alameda relished buying and selling again in the day, one with low float and excessive FDV.

Buying and selling in the pre-launch markets has been fairly energetic. Binance has almost $250 million in open curiosity (OI) and over $500 million in 24-hour buying and selling quantity. Hyperliquid has seen over ~1.5 billion WLFI commerce on platform and has ~$60 million in OI. Pre‑launch markets ought to at all times be taken with a grain of salt, due to structural weaknesses: value is a consensus amongst contributors with out an exterior spot oracle, so market energy can drive prints. That dynamic was on show this week when a nicely‑capitalized dealer blew out the Hyperliquid XPL pre-market, roughly tripling the worth in a brief window and triggering widespread liquidations of shorts. Funding on Hyperliquid “hyperps,” and broadly all pre-launch markets, is calculated from a transferring common of closing costs quite than an exterior spot reference, which might amplify these episodes.

A primary‑wave float in the $0.20–$0.42 vary equates to a number of hundred million {dollars} to over $1 billion of notional tokens crossing into circulation. Such scale sometimes produces huge foundation swings and funding skews because the spot markets open and cross‑venue liquidity rebalances. As spot buying and selling commences, the cross-exchange foundation ought to compress, however not with out volatility. Whereas buying and selling has been vigorous, the size of the unlock can nonetheless eclipse present pre-market OI and trigger large value swings.

Taking a step again from the numbers, it’s vital to recollect what the WLFI token represents. WLFI’s “gold paper” phrases state the token is for governance solely: no income, no distributions, no fairness, and no rights to protocol money flows. The identical phrases disclose a hard and fast grant of twenty-two.5 billion WLFI to DT Marks DeFi, LLC (affiliated with Donald J. Trump) and a income‑sharing settlement that routes 75% of web protocol revenues to that entity and 25% to different insiders—outdoors of the tokenholder base. WLFI governance votes are for signaling solely and may be overturned by the World Liberty group at their discretion. Essentially the most worthwhile enterprise of World Liberty Monetary to date, its USD1 stablecoin (coded by Binance), launched with out a discussion board publish or governance vote.

In case you are a memecoin dealer or a charges dealer, good luck. In case you are extra involved with fundamentals, re-read the paragraph above. – Thad Pinakiewicz

Google Enters the Company Blockchain Race

This week, Google announced its layer-1 (L1) chain, Google Cloud Common Ledger (GCUL). This was the third company blockchain announcement in simply two weeks (following Circle’s Arc and, informally, Stripe’s Tempo), and the fourth since Robinhood’s announcement in June.

Google mentioned extra technical particulars shall be introduced in the approaching months, however we do know a number of vital bits of knowledge. For starters, we all know the chain is “Google-developed,” non-public and permissioned (for now), will assist Python-based sensible contracts, and has a transparent give attention to funds and asset issuance. The corporate went to nice lengths to precise its optimism about blockchains and funds, publishing a blog post titled “Past stablecoins: The evolution of digital cash.” The write-up particulars the historical past of cash from privately issued banknotes in the 1700s to stablecoins in the present day, the shortfalls of legacy digital infrastructure associated to funds and capital markets at giant, and the way GCUL (or distributed ledgers usually) is positioned to fill the gaps and create new potentialities. It emphasizes that the mix of digitized {dollars} and distributed ledgers can ship important developments without having to reinvent the idea of cash or markets, enabling nice strides in functionality and effectivity via evolution quite than revolution.

Google’s weblog publish, mixed with the recruitment of CME as a pilot accomplice for the chain, underscores that the chain’s focus shall be on funds and asset transfers. It’s additionally vital to notice {that a} central a part of the GCUL pitch is safety and privateness, to be bootstrapped by Google-specific applied sciences.

OUR TAKE:

Google getting into the world is one other signal that we’re firmly in the period of company blockchains. These bulletins have obtained blended critiques from crypto natives.

Robinhood’s Arbitrum Orbit Chain was nicely obtained by the neighborhood, whereas Arc and Tempo have been met with skepticism. GCUL appeared to fly beneath the radar, probably as a result of Google’s important announcement was posted on LinkedIn, and it’s unclear if the corporate will undertake current blockchain infrastructure (e.g., the Ethereum Digital Machine).

The detrimental opinions of these in the neighborhood possible stem from two sources: 1) these company chains not exhibiting “alignment” with belongings and architectures most well-liked by crypto natives, and a couple of) crypto natives’ jaded reminiscences of the enterprise blockchain wave of 2014-2019.

From the alignment perspective, there are two adjoining the explanation why crypto natives have seen company chains like Arc with skepticism whereas cheering on company chains like Robinhood Chain: 1) the technical design of the introduced networks, and a couple of) their exclusion of crypto-native belongings. Crypto natives are passionate in regards to the expertise they’ve constructed, and the neighborhood has performed a central position in the formation of the trade at giant. Companies leaning on the tech however not constructing out options, as these in the trade suppose is finest, have probably pressed some buttons. This was obvious in the reward of Robinhood’s venture (an L2) and the skepticism of Arc (an L1). Furthermore, not together with the crypto-native belongings of sure tech stacks whereas utilizing parts of them (e.g., constructing on the EVM however ignoring ETH) might need poured fuel on the flames. This was obvious in the reward of Robinhood, which must pay charges to the Ethereum L1, and skepticism of Arc, which shall be powered by a stablecoin.

Critiques framed solely round structure and asset alternative miss the purpose. What finally issues is whether or not these chains uphold ideas of decentralization and promote particular person sovereignty (e.g., self-custody) in the identical means some public chains can. Judged on these traces, company chains can play a constructive position in introducing giant teams of recent customers to crypto infrastructure (e.g., wallets), which is way extra consequential than whether or not they function as an L1 or an L2 or on the EVM or its Solana equal, and may introduce extra individuals to the belongings.

From the historic perspective, the conflict of crypto-natives and companies constructing on blockchains goes again a minimum of a decade. This pattern was tried earlier than, and clearly by no means amounted to a lot. Many of the company chains constructed in the previous have been “enterprise blockchains,” which have been considerably much less blockchain-like than a number of the options introduced during the last couple of months. Differentiating components vary from the not too long ago introduced chains supporting sensible contracts, permitting them to host purposes, supporting asset issuance, to their going through finish customers, so people can work together with the chain. This mix of traits was uncommon in enterprise blockchains of the previous, which targeted on practices resembling provide chain administration and logistics and have been by no means actually used instantly by shoppers.

Though crypto natives have critiqued points of the not too long ago introduced company chains, a number of the panned design decisions have been intentional and partially pushed by safety and privateness. Within the Arc litepaper, Circle cited issues across the transparency of public chains being at odds with required confidentiality for real-world monetary exercise and the potential for settled transactions to be rolled again on the discretion of the chain’s governance process (which the company can’t management).

Privateness and safety have been additionally central to the pitch for GCUL, which included its simplicity, flexibility, and security. Notably, Google has baked neutrality into its advertising supplies for GCUL, suggesting the corporate is making an attempt to make use of its lack of alignment with any established belongings or structure as a power to draw a bigger group of potential builders and customers. – Zack Pokorny

Crypto Coalition to Congress: No Dev Protections, No Invoice

On Wednesday, the DeFi Schooling Fund sent a letter to the Senate Banking and Agriculture Committees urging lawmakers to prioritize sturdy nationwide protections for software program builders and non-custodial service suppliers in digital asset market construction laws. Co-signed by greater than 110 organizations (together with Galaxy), the letter made clear that, absent such protections, the signatories couldn’t assist a market construction invoice.

The letter argues that builders and non-custodial service suppliers shouldn’t be pressured into “unworkable regulatory classes” designed for conventional intermediaries. As an alternative, laws should acknowledge open-source improvement as impartial infrastructure, persevering with the longstanding U.S. custom of safeguarding software program innovation. The letter highlights the chance of ceding management, noting that America’s share of open-source builders has already fallen from 25% in 2021 to 18% in 2025, a decline attributed largely to regulatory uncertainty.

Whereas the Home and Senate have already superior measures just like the Blockchain Regulatory Certainty Act (BRCA) and Preserve Your Cash Act (KYCA), the coalition confused that further clarifications and federal preemption are important. They name for express statutory language making certain that people engaged in creating, publishing, or sustaining blockchain software program, in addition to these offering non-custodial interfaces, aren’t regulated as monetary intermediaries. With out this readability, the coalition warns, innovation dangers being pushed offshore, weakening U.S. competitiveness in the digital economic system.

The DeFi Schooling Fund is a analysis and advocacy group that works to bridge understanding between the DeFi neighborhood and policymakers, simplifying decentralized finance for regulators and pushing for clearer, balanced coverage frameworks whereas defending builders and open-source builders. It was based in 2021 following a Uniswap governance vote to fund advocacy and lobbying for the DeFi sector with an preliminary funding of 1 million UNI tokens.

OUR TAKE:

As progress is made in Washington towards complete crypto laws, the letter highlights a key excellent space of debate: how you can present clear protections for builders and non-custodial service suppliers so america can preserve its management in open-source innovation. By demanding that builders and non-custodial suppliers not be regulated as cash transmitters, the letter pushes lawmakers to transcend current proposals, making certain that protections are clear, uniform, and binding on the federal degree.

The timing of the letter is very important contemplating current enforcement circumstances. The conviction of Roman Storm, co-founder of Twister Money, on expenses of conspiracy to function an unlicensed money-transmitting enterprise, highlighted the dangers builders face when constructing non-custodial protocols (coated by Galaxy Analysis here beforehand). The letter’s message, “no developer protections, no invoice,” goals to get forward of those points now. Whereas the Division of Justice has not too long ago signaled it doesn’t intend to pursue comparable prosecutions in opposition to purely non-custodial builders, the letter argues that discretion isn’t sufficient. As an alternative, Congress should legislate clear protections so innovators can construct with confidence.

Different previous circumstances illustrate the stakes. In CFTC v. Ooki DAO, the courtroom allowed regulators to pursue a decentralized autonomous group as an unincorporated affiliation, elevating legal responsibility dangers for builders and governance contributors. The Commodity Futures Buying and selling Fee’s 2023 settlements with Opyn, Deridex, and 0x handled protocol builders as accountable for unregistered derivatives choices, whereas earlier Securities and Alternate Fee actions, resembling SEC v. EtherDelta, imposed change operator obligations on particular person builders. Litigation round bZx and Ooki DAO has additionally raised the specter of non-public legal responsibility by treating DAO contributors as normal companions. In every occasion, regulators and courts have blurred the road between software program writers and monetary intermediaries. The coalition’s push for express federal protected harbors seeks to reverse that drift and anchor developer protections in statute.

Lastly, the letter displays the rising political footprint of the crypto trade in Washington. Alongside established organizations just like the Blockchain Affiliation and Chamber of Digital Commerce, newer entrants such because the Solana Coverage Institute, Stand with Crypto, and quite a few state blockchain crypto councils signed on, exhibiting that particular person ecosystems and grassroots teams at the moment are standing up coverage arms of their very own and advocacy is maturing right into a coordinated and institutionalized presence able to mobilizing greater than 100 signatories round a single concern. – Lucas Tcheyan

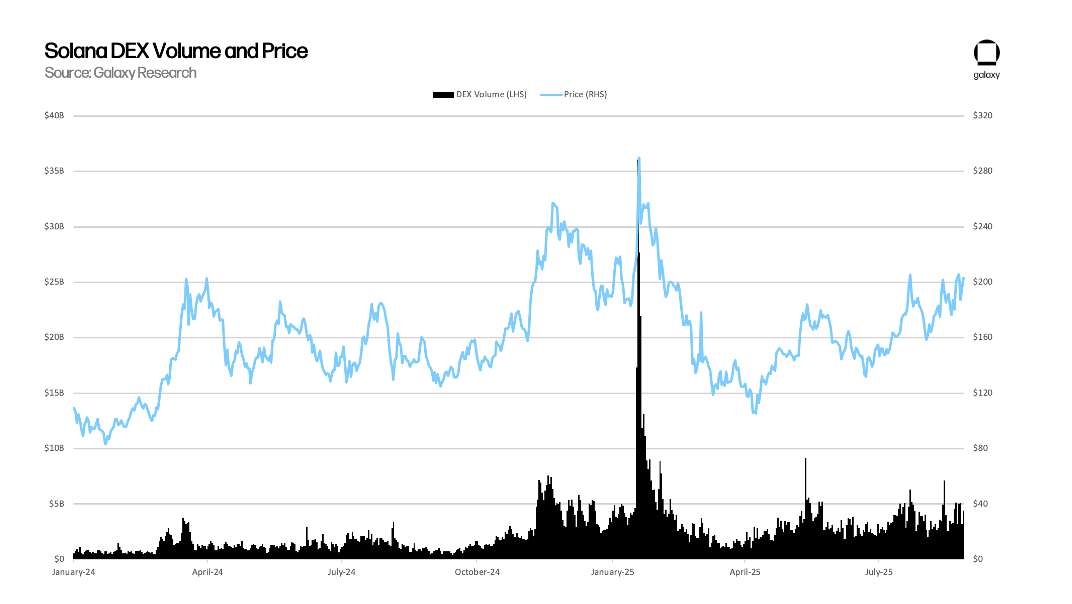

Chart of the Week

Regardless of chatter that Solana’s DeFi “trenches” are dying, decentralized change (DEX) volumes have held regular in the $3 billion to $6 billion each day vary and have trended upward since March.

Different Information

🐦⬛ Trump Media, Crypto.com to build $6.4B CRO treasury agency

🐋 Hyperliquid to add safeguards following whale-driven XPL pre-market liquidations

🔮 Donald Trump Jr.’s VC invests ‘double-digit hundreds of thousands’ in Polymarket

⛓️💥 Prediction market Kalshi to expand onchain presence

💰Union Sq. Ventures leads $15M round for brand spanking new onchain prediction market

👀 U.S. Commerce Division to put economic data onchain by way of ChainLink and Pyth

👔 JPMorgan backs hedge fund Numerai with $500M, fueling crypto-AI convergence

🤖 Anthropic: Criminals are weaponizing AI with assist from bitcoin

🌏 Treasury sanctions crypto IT rip-off spanning North Korea, Russia, and China

⚡ Hut 8 to build 4 new websites with greater than 1.5 GW of capability

Authorized Disclosure:

This doc, and the data contained herein, has been supplied to you by Galaxy Digital Inc. and its associates (“Galaxy Digital”) solely for informational functions. This doc will not be reproduced or redistributed in complete or in half, in any format, with out the specific written approval of Galaxy Digital. Neither the data, nor any opinion contained in this doc, constitutes a proposal to purchase or promote, or a solicitation of a proposal to purchase or promote, any advisory providers, securities, futures, choices or different monetary devices or to take part in any advisory providers or buying and selling technique. Nothing contained in this doc constitutes funding, authorized or tax recommendation or is an endorsement of any of the stablecoins talked about herein. It’s best to make your individual investigations and evaluations of the data herein. Any selections primarily based on data contained in this doc are the only real accountability of the reader. Sure statements in this doc replicate Galaxy Digital’s views, estimates, opinions or predictions (which can be primarily based on proprietary fashions and assumptions, together with, in specific, Galaxy Digital’s views on the present and future marketplace for sure digital belongings), and there’s no assure that these views, estimates, opinions or predictions are at the moment correct or that they are going to be finally realized. To the extent these assumptions or fashions aren’t appropriate or circumstances change, the precise efficiency could fluctuate considerably from, and be lower than, the estimates included herein. None of Galaxy Digital nor any of its associates, shareholders, companions, members, administrators, officers, administration, staff or representatives makes any illustration or guarantee, specific or implied, as to the accuracy or completeness of any of the data or every other data (whether or not communicated in written or oral type) transmitted or made obtainable to you. Every of the aforementioned events expressly disclaims any and all legal responsibility referring to or ensuing from using this data. Sure data contained herein (together with monetary data) has been obtained from revealed and non-published sources. Such data has not been independently verified by Galaxy Digital and, Galaxy Digital, doesn’t assume accountability for the accuracy of such data. Associates of Galaxy Digital could have owned, hedged and bought or could personal, hedge and promote investments in a number of the digital belongings, protocols, equities, or different monetary devices mentioned in this doc. Associates of Galaxy Digital might also lend to a number of the protocols mentioned in this doc, the underlying collateral of which could possibly be the native token topic to liquidation in the occasion of a margin name or closeout. The financial results of closing out the protocol mortgage might instantly battle with different Galaxy associates that maintain investments in, and assist, such token. Besides the place in any other case indicated, the data in this doc is predicated on issues as they exist as of the date of preparation and never as of any future date, and won’t be up to date or in any other case revised to replicate data that subsequently turns into obtainable, or circumstances current or adjustments occurring after the date hereof. This doc offers hyperlinks to different Web sites that we predict is likely to be of curiosity to you. Please observe that once you click on on one in every of these hyperlinks, you might be transferring to a supplier’s web site that isn’t related to Galaxy Digital. These linked websites and their suppliers aren’t managed by us, and we aren’t accountable for the contents or the right operation of any linked website. The inclusion of any hyperlink doesn’t suggest our endorsement or our adoption of the statements therein. We encourage you to learn the phrases of use and privateness statements of those linked websites as their insurance policies could differ from ours. The foregoing doesn’t represent a “analysis report” as outlined by FINRA Rule 2241 or a “debt analysis report” as outlined by FINRA Rule 2242 and was not ready by Galaxy Digital Companions LLC. Equally, the foregoing doesn’t represent a “analysis report” as outlined by CFTC Regulation 23.605(a)(9) and was not ready by Galaxy Derivatives LLC. For all inquiries, please electronic mail [email protected]. ©Copyright Galaxy Digital Inc. 2025. All rights reserved.

{kind=link}