Unlock the Editor’s Digest free of charge

Roula Khalaf, Editor of the FT, selects her favorite tales on this weekly publication.

Crypto works a bit like Candyman: say the title usually sufficient and one thing may seem from nothing.

This not-particularly-virtuous circle of token costs and a focus looking for is a factor we discuss very often. A 12 months in the past, for instance, it by some means turned a matter of worldwide significance that ethereum was going to change its blockchain validation method:

Why are we all speaking about it? The same old motive: crypto values correlate with publicity. Social media noise can push token costs round (Tandon et al), however not as successfully as mainstream media protection (Coulter). Essentially the most highly effective crypto worth accelerant is a positive-sounding theme from an influential supply that’s encouraging to a silent majority (Mei et al). It’s subsequently instantly in the pursuits of ethereum whales (Coinbase, Binance, Kraken etc) to make The Merge look like a really huge deal, and we in the generalist press have been glad to oblige.

This 12 months’s ethereum Merge is the spot bitcoin ETF.

Two months in the past a US judge said it was “arbitrary and capricious” that the SEC permits bitcoin futures ETFs whereas blocking ETFs that maintain bitcoin. The ruling will most likely power the SEC to approve spot bitcoin ETFs as a result of its solely different choice, withdrawing earlier approvals of futures ETFs, can be even more embarrassing.

The SEC’s defeat has been portrayed as an enormous deal for bitcoin, whose worth correlates moderately properly with how usually individuals say bitcoin. The beneath chart exhibits the greenback spot worth alongside volumes of Google searches for bitcoin and articles mentioning bitcoin:

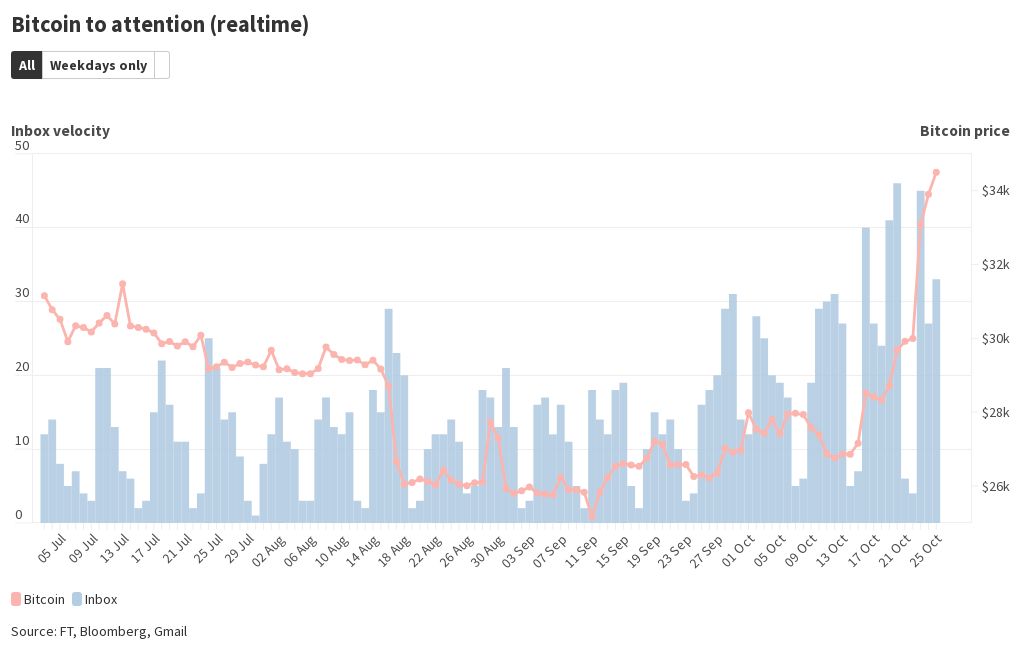

And for a real-time measure, chart two exhibits the bitcoin spot worth versus the variety of emails in the writer’s inbox that reference bitcoin:

Since August 28, the day earlier than the SEC misplaced, bitcoin has added $168bn in market cap. Bitcoin’s 32 per cent achieve over the interval far exceeds that of gold (+3.7 per cent), the Nasdaq Composite (-6.5 per cent) and ethereum (+14.4 per cent, most likely on hopes of US regulators changing into friendlier to crypto), so the foremost driver does look like ETF hype.

To place $168bn in context, there’s $198bn currently invested in spot gold ETFs.

So are retail punters ingesting the crypto Kool-Help once more? Apparently not. Latest bitcoin demand seems to be to be institutional, in line with JPMorgan. Whereas consideration measures like the Google Tendencies rating have been flatlining since crypto winter, open curiosity in CME bitcoin futures contracts (used principally by institutional traders) has spiked again to ranges final seen in August 2022 earlier than the collapse of FTX.

JPMorgan additionally highlights a current tick larger in on-chain transfers from small wallets to huge ones, as proven by the beneath chart. Bitcoin circulation tends to go in direction of the huge wallets when there’s one thing positive-sounding for establishments to promote — corresponding to the launch of the first US futures ETF in 2021 and the halving event of 2020 — then reverses after stuff blows up:

Latest bitcoin demand subsequently seems to be like preparatory work for the ETF advertising and marketing blitz. And since shopping for makes the worth go up, it’s preparation that’s self-propelling.

The SEC has till January 10 to reply to a joint utility from Ark Make investments and 21Shares, although nobody in the business appears to anticipate it to take that lengthy. Grayscale and BlackRock have made formal registrations to launch spot ETFs and right here’s a circulation of filings amendments, indicating back-and-forth between the regulator and asset managers to work out who can maintain what.

It’s seemingly, says JPMorgan, that the SEC will challenge mass approval notices to keep away from gifting any supervisor a first-mover benefit.

The principle advantage of a spot ETF is that it’s a more direct type of possession than an artificial fund, whose reliance on derivatives can introduce lag and hedging risk. A cleaner construction is sweet, however to any potential purchaser of a bitcoin ETF it won’t matter all that a lot. Nobody buys crypto for its simplicity.

Nikolaos Panigirtzoglou, of JPMorgan’s world markets technique staff, has known as the spot benefit “slightly marginal” and “unlikely to be a game-changer for crypto markets”.

Panigirtzoglou additionally highlights the lack of curiosity in spot bitcoin ETFs that already exist.

We’ve discovered 29 bitcoin ETFs globally that would moderately be described as energetic, in addition to 11 exchange-traded notes and 11 exchange-traded commodities. (Right here’s an explainer of what those letters mean, the essence of which is that ETFs are fairness devices and the different two are more like debt. For the functions of this train we’re bunching them collectively.)

Throughout the total group there’s $5.6bn in fund belongings. Of that complete, roughly $3.1bn is in funds that are (or say they are) bodily backed by bitcoin. The remaining $2.5bn is in artificial funds/thriller packing containers.

Right here’s a clickable breakdown by worth, sort and supplier. Be aware nonetheless that for a lot of smaller funds, and some of the bigger ones, the replication methodology wasn’t made clear in the reality sheet; tell us about any errors.

One other helpful measure is shares excellent. As a result of ETFs are open-end funds, their share counts give a sign of demand that’s impartial of asset worth.

The beneath chart exhibits shares in challenge for the Function bodily ETF (in its unhedged Canadian greenback flavour) alongside ProShares’ artificial ETF. Function loved a rush of curiosity round the launch, adopted by two years of nothing a lot:

We’re being advised loads that US-listed spot bitcoin ETFs can be revolutionary for institutional possession of crypto. Going by the historic demand illustrated above, they most likely received’t even be revolutionary for ETF suppliers. Possibilities are that by subsequent 12 months it will all be forgotten, by which period there can be one other bitcoin halving occasion to stay up for.

However when there’s a complete new market to cantillate into existence, who has time to look backwards?