1 Introduction

The notion of blockchain interoperability is gaining important traction each in tutorial analysis and industrial functions. Belchior et al. (2022a) illustrate this development by noting a considerable improve in Google Scholar search outcomes, from two in 2015 to 207 in 2020. This surge in analysis curiosity underscores the rising business demand for interoperability amongst many current blockchains. Traditionally, particular person blockchains had been developed to handle particular use circumstances and challenges in isolation, neglecting cross-chain interoperability (Abebe et al., 2019; Jin et al., 2018). The adaptability of a blockchain to the necessities of its stakeholders has emerged as a vital driver behind the proliferation of recent and numerous blockchains, leading to a heterogeneous blockchain ecosystem and consequent fragmentation of the blockchain panorama (Belchior et al., 2022b; Pillai et al., 2020; Xu et al., 2017). Presently, practitioners and researchers are confronted with the problem of balancing novelty and stability as they contemplate blockchain interoperability to reinforce the scalability of current programs and unlock new use circumstances (Belchior et al., 2022a).

In monetary markets, blockchain know-how finds important software in cryptocurrencies, the place digital tokens are considered as monetary property with potential financial use. Among the many huge array of cryptocurrencies tracked throughout quite a few exchanges, together with Bitcoin (BTC), Ethereum (ETH), Tether (USDT), Binance (BNB), Solana (SOL), and Ripple (XRP), the highest six cryptocurrencies dominate the market shares. As of 18 March 2024, these cryptocurrencies collectively maintain 77.1% of the market capitalization, with Bitcoin alone accounting for 49.4%. Given its substantial market share, the Bitcoin blockchain is a first-rate candidate for internet hosting different blockchains. On this context, bitcoin cross-chain interoperability refers back to the functionality of cryptocurrencies to be exchanged with each other over the Bitcoin blockchain.

Wegner (1996) defines interoperability as the power of a number of software program elements to collaborate successfully regardless of variations in language, interface, and execution platform. The Nationwide Interoperability Framework Observatory (NIFO) (European Commission, 2020) identifies seven layers of interoperability: technical, semantic, organizational, authorized, built-in public service governance, and interoperability governance. Varied components influencing interoperability are categorized inside every layer (Campmas et al., 2022). Whereas present efforts primarily concentrate on the technical layer, we think about semantic-level interoperability. For instance, facilitating a transaction from Ethereum to a Ripple person includes at the least two blockchains: the supply blockchain, Ethereum, and the goal blockchain, Ripple.

The method of transferring property throughout totally different blockchains includes three basic steps: (i) locking an asset on the supply blockchain, (ii) committing to the blockchain switch, and (iii) making a illustration of the asset (often known as a token) on the goal blockchain (Belchior et al., 2022b; Hargreaves et al., 2021). Belchior et al. (2022a) distinguish transfers between heterogeneous blockchains as cross-blockchain communication (CBC), contrasting with cross-chain communication (CCC) between homogeneous blockchains. Zamyatin et al. (2021) show that no CCC protocol can tolerate misbehaving nodes with no trusted third occasion. The selection of a trusted third occasion presents two choices: centralized or decentralized (Montgomery et al., 2020). A centralized trusted occasion could possibly be an alternate or establishment. Zamyatin et al. (2021) recommend that consensus amongst all distributed ledgers could possibly be an abstraction for a trusted third occasion. Conversely, a decentralized trusted occasion could possibly be one other blockchain. Borkowski et al. (2018) suggest that the supply blockchain ought to replicate the consensus mechanism of the goal blockchain. Lafourcade and Lombard-Platet (2020) argue that attaining absolutely decentralized blockchain interoperability is impractical. These findings underscore an important realization: Cross-blockchain transactions necessitate a trusted third occasion, which can contain establishments or consensus mechanisms from the blockchains concerned.

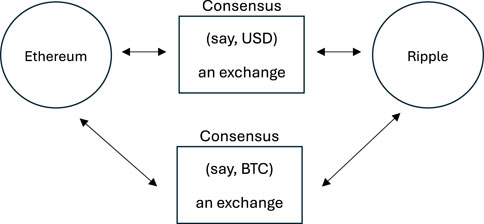

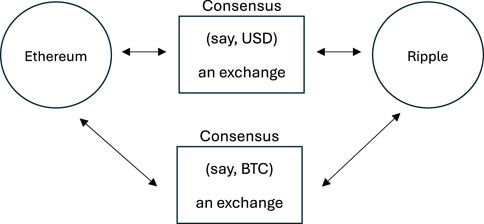

We talk about two situations for establishing third-party consensus: Cryptocurrency exchanges may use both {dollars} or bitcoins to facilitate cross-blockchain transactions. For instance, Ethereum and Ripple transactions can observe two distinct paths (see Figure 1). The primary path includes using a fiat forex, such because the U.S. greenback, as an middleman to facilitate the consensus processes in each the Ethereum and Ripple blockchains. As an example, one Ether could also be valued at $3,480, and with the help of an alternate, $3,480 could possibly be exchanged for five,800 Ripples. This course of establishes an alternate charge between Ethers and Ripples, known as the cross-blockchain (CBC) alternate charge for Ripple by way of Ether, denoted ETHXRP. The second path includes using one other blockchain, such because the Bitcoin blockchain, because the middleman to finish the consensus between Ethereum and Ripple. This strategy leads to two distinct CBC alternate charges, ETHBTC and XRPBTC, together with the Bitcoin-derived CBC alternate charge, BETHXRP. Subsequently, for cross-blockchain transactions between Ethereum and Ripple, there are at the least two varieties of CBC alternate charges, contingent upon the selection of fiat forex or blockchain used. The fiat-currency-derived CBC alternate charge, particularly ETHXRP, serves as a reference level for investigating Bitcoin cross-blockchain interoperability, as BETHXRP represents.

Determine 1. The cross-blockchain transactions between Ethereum and Ripple, showcasing two distinct paths.

It’s noticed that the proposed CBC transaction mannequin may be simplified right into a midway mannequin. Because of this utilizing ETHUSD represents the direct path of a CBC transaction whereas using the bitcoin-derived ETHUSD, denoted as BETHUSD = ETHBTC × BTCUSD, signifies the oblique path of a CBC transaction. The benefit of this strategy is that it permits specializing in one cryptocurrency in opposition to bitcoin at a time.

This examine goals to discover the interoperability of the Bitcoin blockchain with the highest 5 cryptocurrencies by way of market capitalization: ETH, USDT, BNB, SOL, and XRP. The methodology includes evaluating the costs of those 5 cryptocurrencies, specifically, ETHUSD, USDTUSD, BNBUSD, SOLUSD, and XRPUSD, with their bitcoin-derived counterparts: BETHUSD, BUSDTUSD, BBNBUSD, BSOLUSD, and BXRPUSD. Tether is probably the most broadly used dollar-pegged stablecoin. Incorporating Tether within the evaluation is worth it due to its worthwhile correlation with Bitcoin (Bianchi et al., 2020) and its famous instability by way of worth, returns, volatility, and buying and selling quantity (Grobys and Huynh, 2022; Hoang and Baur, 2021).

Within the context of cross-blockchain interoperability, Ether’s worth in {dollars}, facilitated by the Bitcoin blockchain, mustn’t persistently deviate from Ether’s greenback worth. Alternatively, the arbitrage return charge, outlined because the distinction between these two costs, mustn’t persistently current predictable patterns. The absence of long-term reminiscence within the arbitrage returns not solely aligns with environment friendly market theories but in addition means that the Bitcoin blockchain can successfully facilitate transactions throughout different blockchains.

Fama’s (1970) environment friendly market speculation (EMH) states that irregular returns solely exist by likelihood and that no particular person can persistently predict future costs utilizing present info. Samuelson’s (1973) martingale mannequin means that successive returns mustn’t exhibit serial dependence. Nevertheless, anomalies can’t merely be dismissed as random errors (Tversky and Kahneman, 1988). Frankfurter and McGoun (2001) argue that anomalies are generic in nature and recommend a sure kind of market effectivity. Latif et al. (2011) discover that calendar, basic, and technical anomalies can result in irregular revenue. Fama (1990) contends that “such anomalies may be defined solely within the context of some specific conditions.”

One instance of an anomaly is the sluggish response of traders to new info. Jegadeesh and Titman (1993) observe that changes to bulletins normally take 12 months, with variations starting from 6 months to 2 years Barberis and Shleifer (2012) attribute this sluggish adjustment to under-reaction and overreaction. As Fama (1998) concludes in his work, “Market effectivity survives the problem from the literature on long-term return anomalies.”

Bariviera et al. (2017) use the detrended fluctuation evaluation (DFA) technique to research Bitcoin’s intraday returns over 5–12 h with 500 knowledge factors. They argue that DFA is best fitted to nonstationary knowledge than the R/S technique, which tends to confuse short-term and long-term reminiscence. Their examine finds that long-term reminiscence shouldn’t be linked to market liquidity and reduces over time. Fousekis and Tzaferi (2021) make the most of frequency connectedness evaluation, a technique launched by Baruník and Křehlík (2018), to look at how shocks in a single stochastic course of have an effect on one other at numerous frequencies, exploring the connection between returns and buying and selling actions. They recommend that asymmetry, characterised as a temporal hyperlink between returns and buying and selling quantity, may be influenced by the energy of spillovers. Assaf et al. (2022) discover long-term reminiscence by using a matrix derived from the wavelet-based multivariate long-memory estimator developed by (Achard and Gannaz, 2016). They uncover important long-term correlations between Bitcoin and 5 different cryptocurrencies. El Alaoui et al. (2019) observe a nonlinear interplay between Bitcoin returns and the expansion charge of buying and selling quantity utilizing multifractal detrended cross-correlation evaluation (MF-DCCA). Stosic et al. (2019) apply the multifractal detrended fluctuation evaluation (MF-DFA) to Bitcoin, concluding that Bitcoin returns don’t exhibit long-term reminiscence however present anti-persistent long-term correlations in quantity modifications.

This examine proposes using the rescaled vary evaluation (R/S) technique and detrended fluctuation evaluation (DFA) to estimate Hurst exponents utilizing sliding home windows. The Hurst exponent is a statistical metric for predictability and is often utilized to evaluate whether or not a time collection displays long-term reminiscence, which manifests as volatility clustering in return time collection (Bariviera, 2017). A better Hurst exponent additionally enhances the accuracy of backpropagation Neural Networks (Qian and Rasheed, 2004). Moreover, Bai-Perron checks for breakpoints complement the Hurst exponent methodology. This examine contributes to the literature by investigating long-term reminiscence in Bitcoin-related arbitrage returns. The evaluation is carried out utilizing the R programming language.

The rest of the paper is structured as follows: Section 2 outlines the dataset and methodology, Section 3 presents the outcomes and dialogue, and Section 4 concludes the paper.

2 Knowledge and methodology

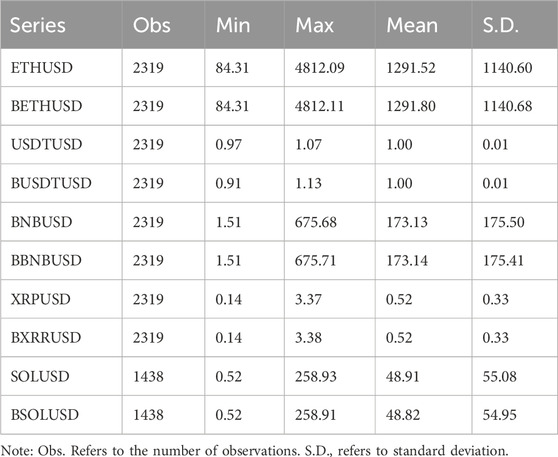

The information is collected each day from Yahoo Finance. This dataset consists of six cryptocurrencies: Bitcoin (BTC), Ethereum (ETH), Tether (USDT), Binance (BNB), Solana (SOL), and Ripple (XRP). Every cryptocurrency has its worth time collection: BTCUSD, ETHUSD, USDTUSD, BNBUSD, SOLUSD, and XRPUSD. Since we use the Bitcoin blockchain because the trusted third-party abstraction, there are 5 cross-blockchain (CBC) alternate charges: ETHBTC, USDTBTC, BNBBTC, SOLBTC, and XRPBTC. For simplicity, we exclude “CBC” from the notation. The investigation interval spans from 11 November 2017, to 18 March 2024, totaling 2319 observations after discarding two lacking values. Nevertheless, Solana, launched in 2020, extends from 10 April 2020, to 18 March 2024, comprising 1438 observations. Utilizing Yahoo Finance as the first knowledge supply for cryptocurrency costs carries the danger of information inaccuracies. Nevertheless, it gives consistency and minimizes timestamp points.

As a way to assess the interoperability of the Bitcoin blockchain, it’s essential to generate a Bitcoin-derived greenback worth for every cryptocurrency, denoted as BCRYPTOUSD. This course of includes evaluating how intently the consensus mechanism of the bitcoin blockchain mirrors that of different cryptocurrency blockchains and, subsequently, the way it interprets this consensus right into a greenback worth inside its personal mechanism. The computation for the bitcoin-derived cryptocurrency worth is printed by Nan and Kaizoji (2017, 2019).

the place “CRYPTO” represents any given cryptocurrency.

As an example, the calculation of BETHUSD on 18 March 2024, may be derived from ETHUSD and ETHBTC utilizing Equation 1:

This means that one ether is valued at $3561 when bridged by the bitcoin blockchain. Notably, ETHBTC was quoted at $3561.764 on the identical day.

Equally, there are 2319 observations for 4 bitcoin-derived cryptocurrency costs: BETHUSD, BUSDTUSD, BBNBUSD, and BXRPUSD, whereas BSOLUSD has 1438 observations.

For every cryptocurrency and US greenback pair, two costs are quoted: one direct worth and one oblique worth bridged by the bitcoin blockchain. The arbitrage return charge between these two costs may be constructed utilizing the equation supplied by Nan and Kaizoji (2020) and Pichl and Kaizoji (2017).

the place

The Hurst exponent, denoted as H, quantifies the diploma of serial dependence in a time collection. Initially developed to measure long-term reminiscence in hydrological time collection by Hurst (1951), it was later launched by Mandelbrot and Wallis (1968) for analyzing monetary time collection. Theoretically, the worth of the Hurst exponent categorizes a time collection into three teams, as outlined by Qian and Rasheed (Qian and Rasheed, 2004): (i) a white noise when 0 < H < 0.5, (ii) a random stroll when H = 0.5, and (iii) a persistent collection when H > 0.5. As H approaches 0, the energy of serial dependence weakens, whereas it strengthens as H approaches 1.

Varied estimators of the Hurst exponent primarily based on scaling properties exist, with two generally used ones being the R/S estimator, which depends on the rescaled vary statistic, and the detrended fluctuation evaluation (DFA) estimator. Moreover, we make use of a sliding window technique to evaluate the dynamics of the estimated Hurst exponents.

2.1 R/S estimator

The rescaled vary evaluation (R/S) technique scales the vary of the cumulative sum of deviation of a time collection from its imply (Bariviera, 2017). Let

(i) Cut up

Every subperiod has an equal size of

Be aware that the subscripts have totally different meanings:

(ii) Calculate the imply

Be aware that the final subperiod

(iii) Calculate the demeaned

the place

(iv) Calculate the cumulative collection of

(v) Discover the vary

(vi) Rescale the vary

(vii) Repeat steps (i) through (vi) by various

The size of the subseries,

the place we purpose for

The R/S statistic is understood to asymptotically observe the relation proven in Equation 4 (Hurst, 1951)

the place

2.2 DFA estimator

The detrended fluctuation evaluation (DFA), launched by Peng et al. (Peng et al., 1995) mitigates spurious detection of long-range dependence (Bariviera, 2017). Not like the R/S technique that measures the utmost vary in each instructions, DFA calculates the typical of the squared vertical distance of

The DFA process includes 5 steps (Penzel et al., 2003).

(i) Decide the cumulative demeaned collection

the place

(ii) Divide

which can lead to a brief section on the finish of the profile. To mitigate its impression, the process is repeated from the other finish, leading to a complete of

(iii) Compute the native development for every subperiod utilizing an OLS regression. Then, decide the variance for every subperiod utilizing Equation 6:

the place

(iv) Acquire the fluctuation perform by taking the sq. root of averaged variances over

(v)Repeat steps (i)-(iv) for various time scale

If the time collection

Equally,

2.3 Sliding window

The sliding window method includes using a set window measurement, denoted as,

This strategy impacts the estimation procedures of R/S and DFA by substituting

3 Outcomes

Table 1 shows the abstract statistics of cryptocurrency and bitcoin-derived cryptocurrency costs. Notably, the bitcoin-derived costs don’t exhibit important deviations from their direct costs relating to minimal, most, imply, and customary deviation. This commentary means that the Bitcoin blockchain’s interoperability maintains unbiasedness from an unconditional statistical perspective.

Desk 1. Abstract statistics of the cryptocurrency costs and their bitcoin-derived costs.

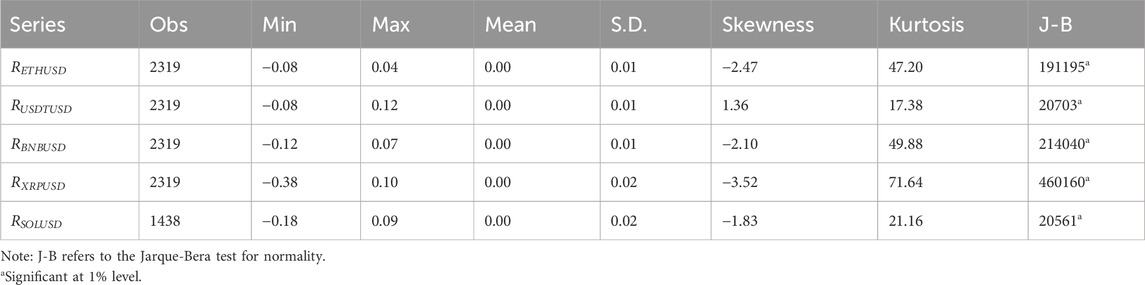

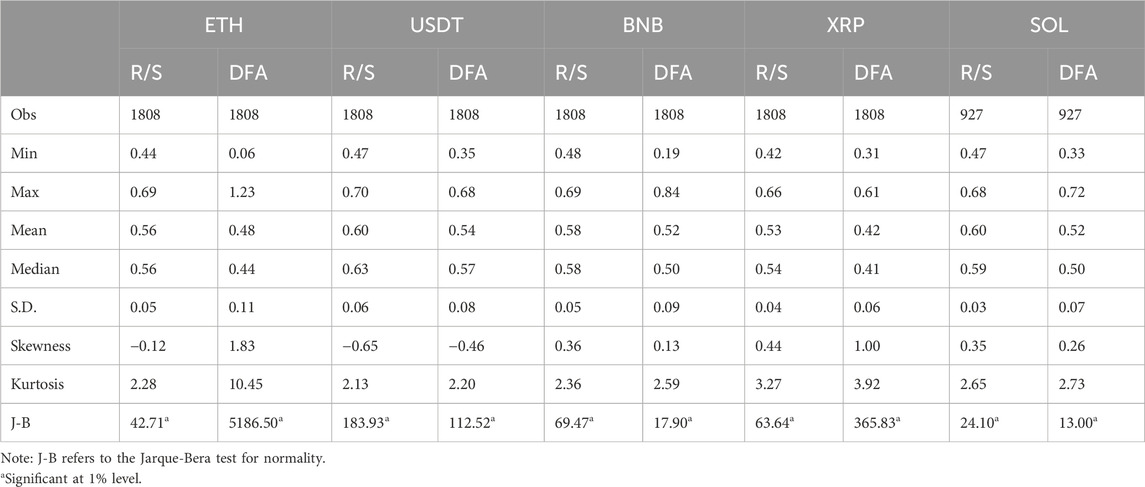

Table 2 gives the descriptive statistics of the return charges related to arbitrage between the bitcoin-derived and direct costs. Whereas the imply of the arbitrage return charges is sort of zero throughout all circumstances, the each day customary deviations vary between 1% and a couple of%, implying that roughly 95% of the info factors exhibit deviations from the imply throughout the vary of −6%–6%. Some excessive values are noticed, corresponding to a 38% adverse deviation for Ripple and a 12% optimistic deviation for USDT. Moreover, these return collection exhibit skewed leptokurtic and non-normal traits.

Desk 2. Abstract statistics of the arbitrage return charges.

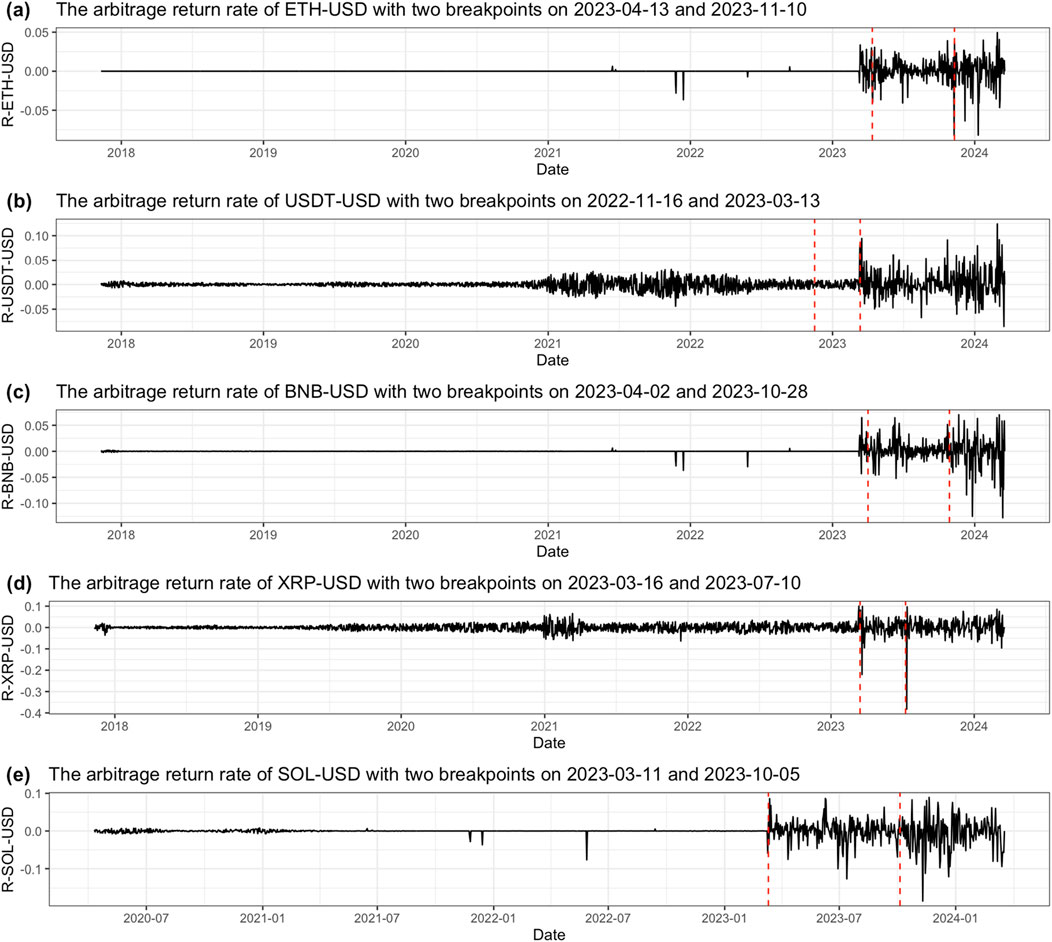

Figure 2 shows the time collection of arbitrage returns, with pink dashed strains indicating breakpoints. Every collection displays a mean-reverting attribute with occasional spikes. Nevertheless, a sudden improve in fluctuation magnitudes was noticed in the direction of the tip of the time collection throughout all 5 cryptocurrencies. We make use of the Bai-Perron check (Bai and Perron, 2003) to determine potential structural modifications in every arbitrage return collection and decide the places of those breakpoints. Two breakpoints are highlighted in Figure 2 with pink dashed strains. Notably, one widespread breakpoint occurred for all 5 return processes between 13 March 2023, and 13 April 2023. These observations elevate questions in regards to the Bitcoin blockchain’s interoperability: Are these fluctuations persistent and predictable? What induced such a change? Partial solutions to those questions lie within the values of the Hurst exponents. Table 3 gives abstract statistics of the Hurst exponents estimates.

Determine 2. The arbitrage returns with potential breakpoints.

Desk 3. Abstract statistics of Hurst estimates.

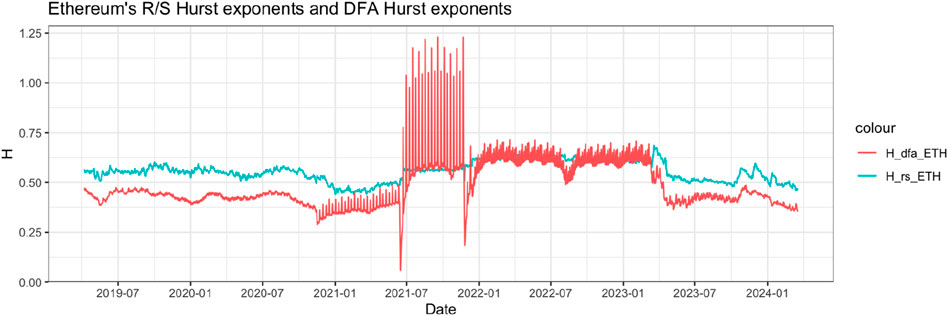

Figure 3 illustrates Ethereum’s Hurst exponents estimated utilizing the R/S and DFA strategies. Each collection exhibit an analogous development, with the R/S estimates largely above the DFA’s. The DFA estimator (H_dfa_ETH) shows elevated volatility within the center part of the collection. These findings recommend that whereas the DFA broadly aligns with the R/S relating to modifications in H values, they diverge by way of their ranges: the R/S tends to overestimate H, whereas the DFA tends to underestimate H however is extra delicate to anomalies. Each strategies point out that Ethereum’s arbitrage return collection lacks sturdy, predictable persistence over the pattern interval: the R/S implies a random stroll course of, whereas the DFA suggests a mean-reverting course of. Nevertheless, from July 2021 to April 2023, the serial dependence strengthened, significantly within the DFA, which displays evident long-term reminiscence regardless of its volatility. Curiously, each estimators return to non-persistent ranges after April 2023, indicating that the extremely oscillating interval within the latter a part of Ethereum’s arbitrage returns (see Panel (a) of Figure 1) doesn’t improve predictability. Although mean-reverting processes may recommend predictability, Fama (1998) concludes that anomalies are likely to reverse, so unpredictability nonetheless holds in the long run.

Determine 3. Ethereum’s R/S Hurst exponents and DFA Hurst exponents.

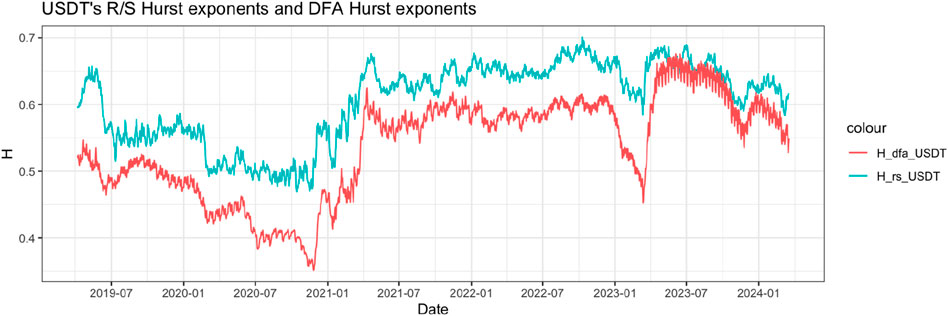

The stablecoin examined in our examine, Tether, has demonstrated important serial dependence energy since April 2021 (discuss with Figure 4). This means that the Bitcoin blockchain encountered challenges in facilitating transactions between USDT customers and U.S. {dollars}. This era of malfunction may result in predictable income. Nevertheless, after the conclusion of 2023, there seems to be a declining development within the estimated Hurst exponents for USDT. Correspondingly, USDT’s arbitrage return conduct exhibited volatility throughout this era.

Determine 4. USDT’s R/S Hurst exponents and DFA Hurst exponents.

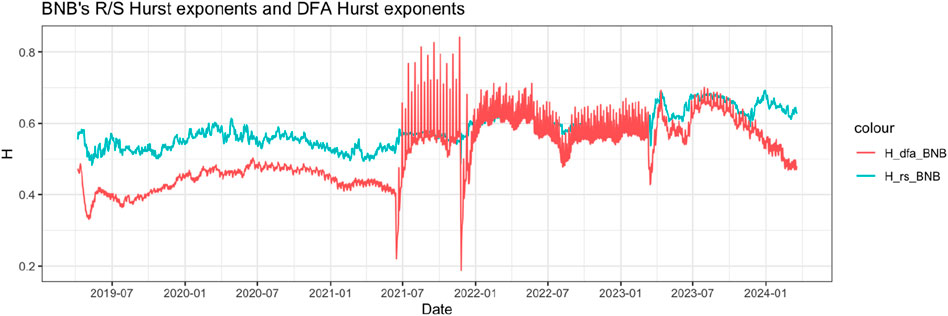

Relating to Binance, the Hurst exponents estimated through the R/S technique point out both a random stroll sample or a restricted degree of serial dependence energy, as depicted in Figure 5. The DFA estimator tended to spotlight a powerful development post-July 2021 however has reverted to indicating a random stroll course of because the onset of 2024.

Determine 5. BNB’s R/S Hurst exponents and DFA Hurst exponents.

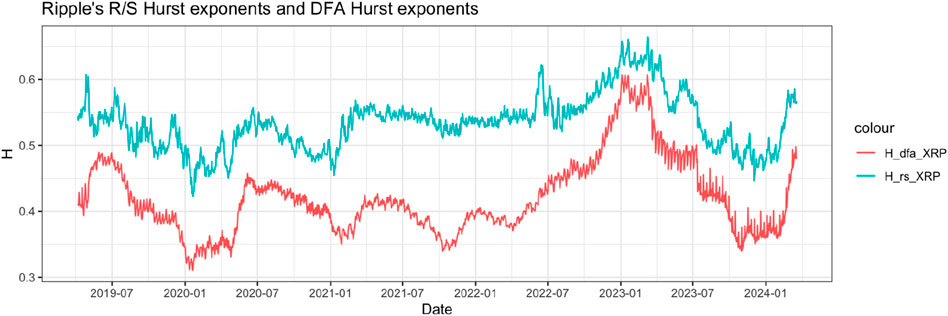

The disparity between the R/S Hurst and DFA Hurst exponents is most pronounced for Ripple’s arbitrage returns, as illustrated in Figure 6. This means that the R/S technique perceives the return sample as extra identifiable and predictable, whereas the DFA considers it white noise. Nevertheless, because the conclusion of 2022, Ripple’s arbitrage returns have exhibited a powerful development, which has dissipated since July 2023. The noticed disparity between these strategies, significantly for Ripple’s arbitrage returns, may be attributed to the distinct sensitivities of every method to several types of knowledge noise and developments. Particularly, the DFA technique mitigates the spurious detection of long-range dependence (Bariviera, 2017).

Determine 6. Ripple’s R/S Hurst exponents and DFA Hurst exponents.

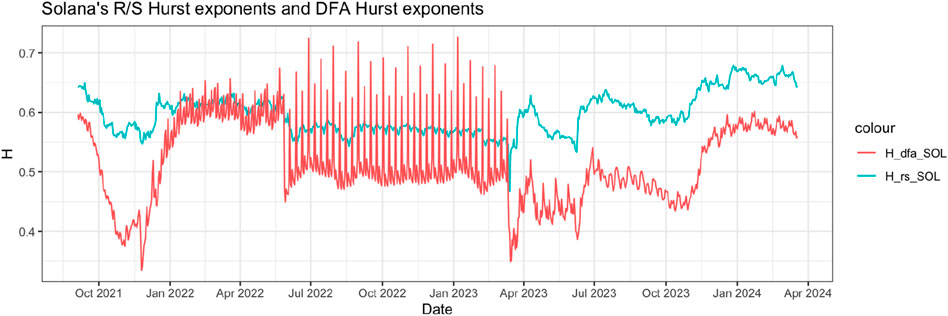

Lastly, Solona’s arbitrage returns demonstrated important persistence from January 2022 to June 2022 (see Figure 7). Afterwards, the DFA Hurst exponents displayed excessive oscillations, suggesting elevated and cyclic predictability from June 2022 to March 2023. Subsequently, there was a divergence between the R/S and DFA estimators. Each estimators indicated the next degree of dependence energy at first of 2024.

Determine 7. Solana’s R/S Hurst exponents and DFA Hurst exponents.

4 Conclusion

Cross-blockchain interoperability is a vital concern for facilitating transactions throughout numerous current cryptocurrencies, with the interoperability closely reliant on a trusted third occasion. One viable possibility is to make the most of a blockchain as this middleman occasion to bridge cross-blockchain transactions. Given its substantial market capitalization, the Bitcoin blockchain is a powerful contender for fulfilling this position, encompassing roughly 50% of the market share. Consequently, our investigation targeted on assessing the interoperability of the bitcoin blockchain with the opposite high 5 cryptocurrencies by market capitalization: Ethereum, Tether, BNB, Solana, and Ripple.

We launched a middle-ground strategy whereby every cryptocurrency is linked to US {dollars} through the Bitcoin blockchain as a substitute of instantly facilitating transactions between two cryptocurrencies. This strategy mitigates ambiguity arising from uneven influences of particular person cryptocurrencies. Subsequently, interoperability was examined by evaluating the greenback worth derived through the Bitcoin blockchain with every cryptocurrency’s “direct” greenback worth. The deviation charge between these two costs served because the arbitrage-return charge. Adhering to environment friendly market theories, we scrutinized whether or not long-term serial dependence existed in all arbitrage-return time collection.

The dynamics of Hurst exponents, estimated utilizing the R/S and DFA strategies, point out weak proof of reminiscence persistence, with traits leaning extra in the direction of a random stroll or white noise sample over our pattern interval from 11 November 2017, to 18 March 2024. These outcomes are in step with Fama’s (1970, 1990) environment friendly market speculation, suggesting that costs observe a random stroll with returns reverting to a trivial imply.

Some sub-periods exhibited pronounced energy of dependence, accompanied by volatility and cyclical conduct. The noticed autocorrelation could originate from a sluggish response to new info (Barberis and Shleifer, 2012). Cyclical conduct, probably brought on by the investor overreaction (De Bondt and Thaler, 1985), aligns with Fama’s (1998) assertion that almost all long-term return anomalies are likely to dissipate, resulting in a sample the place previous winners grow to be future losers and vice versa. In regards to the excessive volatility noticed in all 5 arbitrage return collection after April 2023, Malkiel (2003) concludes his analysis by saying that no matter how excessive the worth volatility is, capital markets should be environment friendly if the worth is much less predictable. These findings recommend that the values of cryptocurrencies passing through the Bitcoin blockchain don’t lead to predictable deviations from the costs decided inside their respective blockchains through their consensus mechanisms.

Consequently, we infer that the semantic layer of the Bitcoin blockchain’s interoperability usually operated successfully, assuming the exclusion of the technical layer and different layers past the scope of this examine. Nonetheless, we noticed a big improve in volatility clustering since April 2023 throughout all cryptocurrencies. These phenomena could stem from structural modifications within the performance of the Bitcoin blockchain. We suggest additional exploration into the potential decreased dependency of different cryptocurrencies on Bitcoin as a subject for future analysis.

Knowledge availability assertion

The unique contributions offered within the examine are included within the article/Supplementary Material, additional inquiries may be directed to the corresponding creator.

Creator contributions

ZN: Conceptualization, Knowledge curation, Formal Evaluation, Funding acquisition, Investigation, Methodology, Mission administration, Assets, Software program, Supervision, Validation, Visualization, Writing–unique draft, Writing–evaluation and enhancing.

Funding

The creator(s) declare that no monetary help was acquired for the analysis, authorship, and/or publication of this text.

Acknowledgments

We’re deeply grateful to the referees for his or her useful options and insightful feedback, which have drastically improved our paper’s high quality and readability.

Battle of curiosity

The creator declares that the analysis was carried out within the absence of any industrial or monetary relationships that could possibly be construed as a possible battle of curiosity.

Writer’s be aware

All claims expressed on this article are solely these of the authors and don’t essentially symbolize these of their affiliated organizations, or these of the writer, the editors and the reviewers. Any product which may be evaluated on this article, or declare which may be made by its producer, shouldn’t be assured or endorsed by the writer.

Supplementary materials

The Supplementary Materials for this text may be discovered on-line at: https://www.frontiersin.org/articles/10.3389/fbloc.2024.1410191/full#supplementary-material

References

Xu, X., Weber, I., Staples, M., Zhu, L., Bosch, J., Bass, L., et al. (2017). A taxonomy of blockchain-based programs for structure design. IEEE Int. Conf. Softw. Archit. (ICSA), 243–252. Obtainable at: https://ieeexplore.ieee.org/abstract/document/7930224/. doi:10.1109/ICSA.2017.33

{kind=link}