Darkish pool HumidiFi has grown to develop into the largest DEX protocol on the Solana blockchain surpassing Meteora, Raydium, and Pump on all fronts.

Abstract

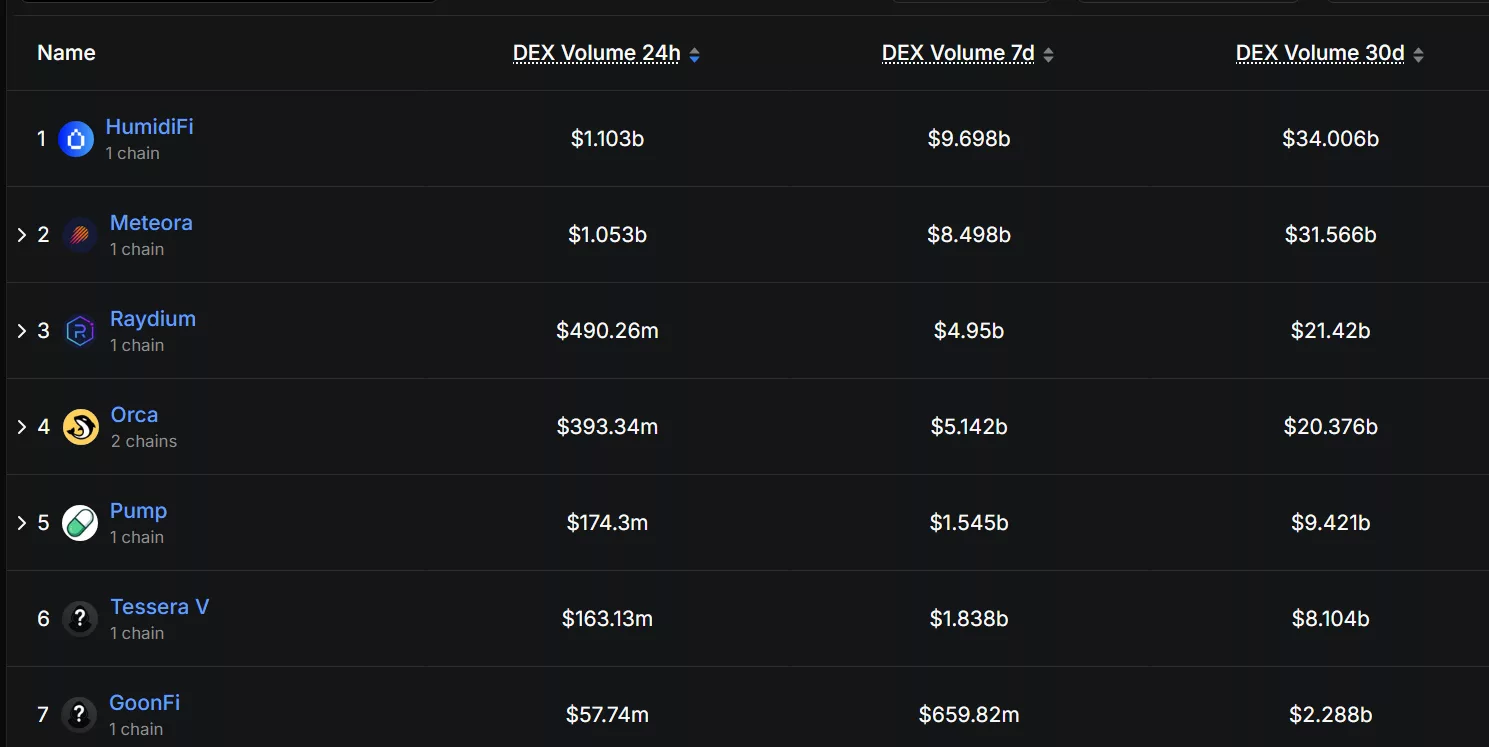

- HumidiFi has overtaken main rivals like Meteora, Raydium, and Pump.enjoyable to develop into Solana’s largest DEX, recording over $1.1 billion in 24-hour buying and selling volume.

- Its rise highlights a broader shift in DeFi towards darkish pool or proprietary AMM fashions that prioritize execution effectivity and privateness over transparency and open liquidity.

On Oct. 20, the darkish pool decentralized change HumidiFi formally turned the largest protocol on the Solana blockchain, having surpassed Meteora, Raydium and Pump.enjoyable. In line with information from DeFi Llama, the protocol contributes as a lot as $1.1 billion to the whole 24 hour DEX buying and selling volume on Solana.

At press time, the whole each day DEX volume on Solana (SOL) has amounted to greater than $3.68 billion. In comparison with Meteora, the second largest DEX on Solana, the darkish pool protocol solely has a $100 million head begin.

When it comes to DEX buying and selling volume inside the previous seven days, it’s also within the lead with a buying and selling volume that has almost reached $10 billion. In the meantime, Meteora’s seven-day buying and selling volume is round $1.2 billion in need of the opposite protocol.

However, Raydium’s (RAY) each day DEX volume is nearing $500 million. Its seven-day buying and selling volume remains to be beneath $5 billion, indicating that it’s nonetheless half-way behind the 2 largest DEX platforms on Solana.

In the meantime, Solana’s meme coin launcpad Pump.enjoyable (PUMP) has fallen removed from grace. The protocol’s DEX buying and selling volume sits at $174.3 million. Regardless of this, Pump.enjoyable’s DEX buying and selling volume has amounted to $1.5 billion whereas its 30-day volume has reached $9.4 billion.

HumidiFi is a decentralized-exchange platform constructed on the Solana blockchain that operates utilizing a “proprietary” automated market maker or prop AMM, relatively than the normal open-liquidity-pool AMM mannequin. Which means the protocol doesn’t depend on exterior liquidity suppliers contributing to open swimming pools the best way many customary AMMs do. Therefore, why it is named a “darkish pool.”

Darkish swimming pools hold trades fully invisible to different customers, not like on conventional exchanges. With protocols like HumidiFi, merchants are capable of execute personal merchants, that are notably helpful for finishing up high-value trades and enormous liquidations.

What does HumidiFi’s surge point out?

The sudden surge of buying and selling exercise on HumidiFi may sign deeper adjustments inside the decentralized finance sector. It signifies a shift in how liquidity is offered and consumed in DeFi.

Conventional DEX fashions, that are recognized for open AMMs and public liquidity swimming pools, are being challenged by fashions the place liquidity is centrally managed and trades are routed through aggregators like Jupiter to excessive‐effectivity venues. This will likely imply that the market is shifting from public swimming pools to darkish swimming pools.

Merchants could also be prioritizing execution effectivity and institutional-grade buying and selling mechanics relatively than conventional metrics like seen whole worth locked or open-pool liquidity. HumidiFi claimed to have processed $8.55 billion in weekly buying and selling volume whereas having a really low TVL, because it emphasizes tight spreads, low slippage and decreased publicity to front-running or sandwich assaults.

However, the rise in HumidiFi’s buying and selling volume may imply that extra merchants are inclined to make their trades nameless as a substitute of public information. The shift towards closed liquidity fashions may very properly elevate considerations about transparency, decentralization, and equity on-chain.

Not solely that, there’s additionally the query of whether or not the mannequin could be sustainable within the long-term. It might be attainable that the surge in exercise is simply quickly motivated by explicit market circumstances or pairs which are being executed on the platform in the mean time.

{kind=link}